State of India EOR 2026

The primary-source research report on Employer of Record in India. PE risk, contractor misclassification, ESOP tax, the real EOR-to-entity crossover, and the $1,800 landed cost reality.

Published: May 2026 · Last updated: 19 May 2026 · ~60 min read · Asanify Research

Contents

This is a research publication of Asanify Research. It is not legal, tax, or other professional advice. Statutory and regulatory positions reflect our understanding as of the cover date and may have changed since publication. Full notices at the end of this report and at asanify.com/research/notices. Corrections: research@asanify.com.

Top 5 Numbers From This Report

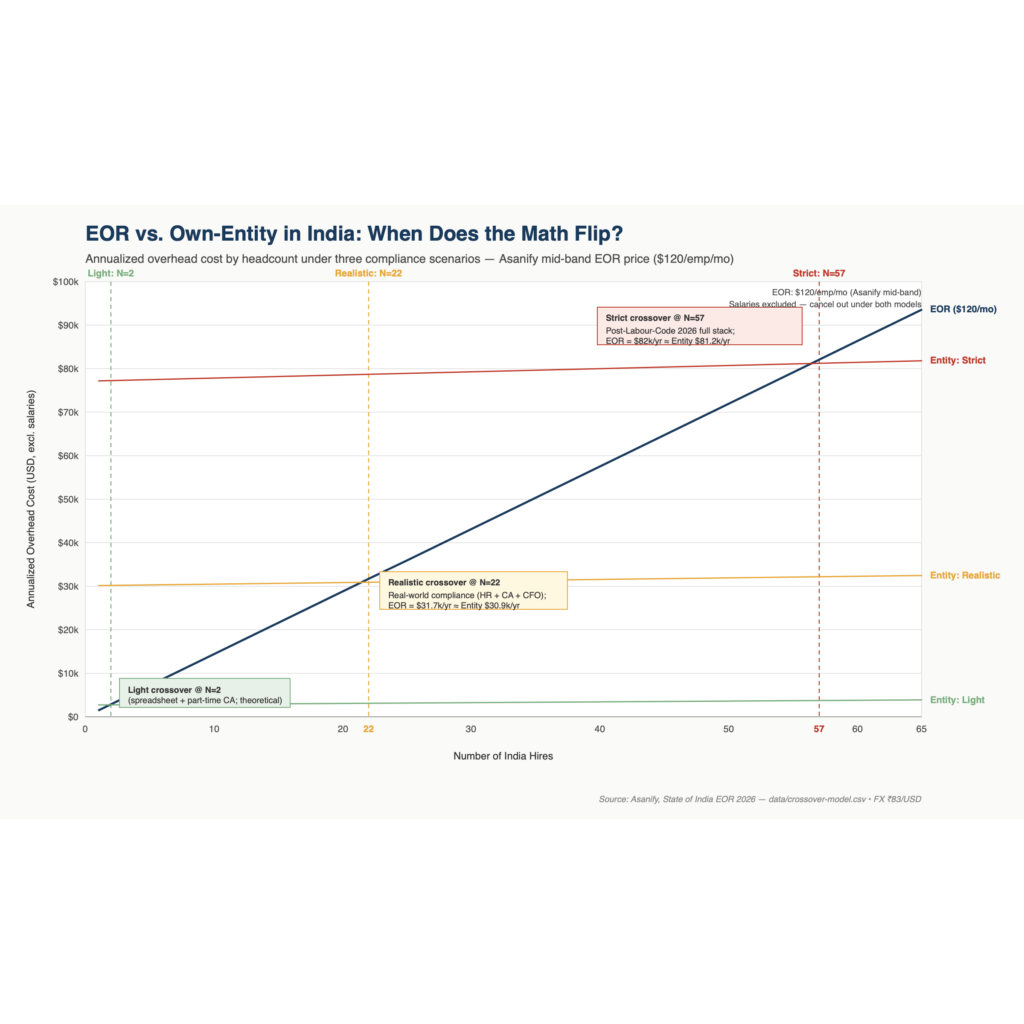

- Financially, your own entity (vs. EOR) may make sense only after you have 50+ employees. We modelled the full cost stack across three compliance scenarios and surfaced a counterintuitive finding: the widely cited ~20–25 employee crossover is off by a factor of 2x. Section B9 shows the math for all three. (Source: Section B9 — EOR vs. Own-Entity Crossover Model)

- Global startups and SMBs regularly use EOR as their India market-entry vehicle — the median global headcount at India EOR sign-on is less than 50 employees. India-specialist EOR is not just for large multinationals executing mature expansion plans. (Source: Asanify proprietary research)

- If you plan to grant stock options to your India EOR team, expect a cash tax bill at the time of exercise — with no delay option. Indian tax law treats the gain at exercise (market price minus exercise price) as salary income, taxable immediately at marginal rates of 30–40%, before any shares are sold. India’s startup tax deferral that delays this bill requires two government certifications that fewer than 2% of India-registered startups hold — and foreign-parented companies, including any US or UK parent, are structurally ineligible. Budget 2026 has not changed this. (Source: Section B5 — ESOPs and Equity for Indian Employees of Foreign Companies)

- Six tribunal and Supreme Court rulings in 18 months — one of the densest stretches of India-EOR-relevant PE jurisprudence in recent history. One Supreme Court ruling (Hyatt) upheld PE; five narrowed the dependent-agent test in ways that favour carefully structured foreign principals. The safe-harbor assumption no longer holds without independent PE analysis. (Source: Section B1 — PE Risk for Foreign EOR Users)

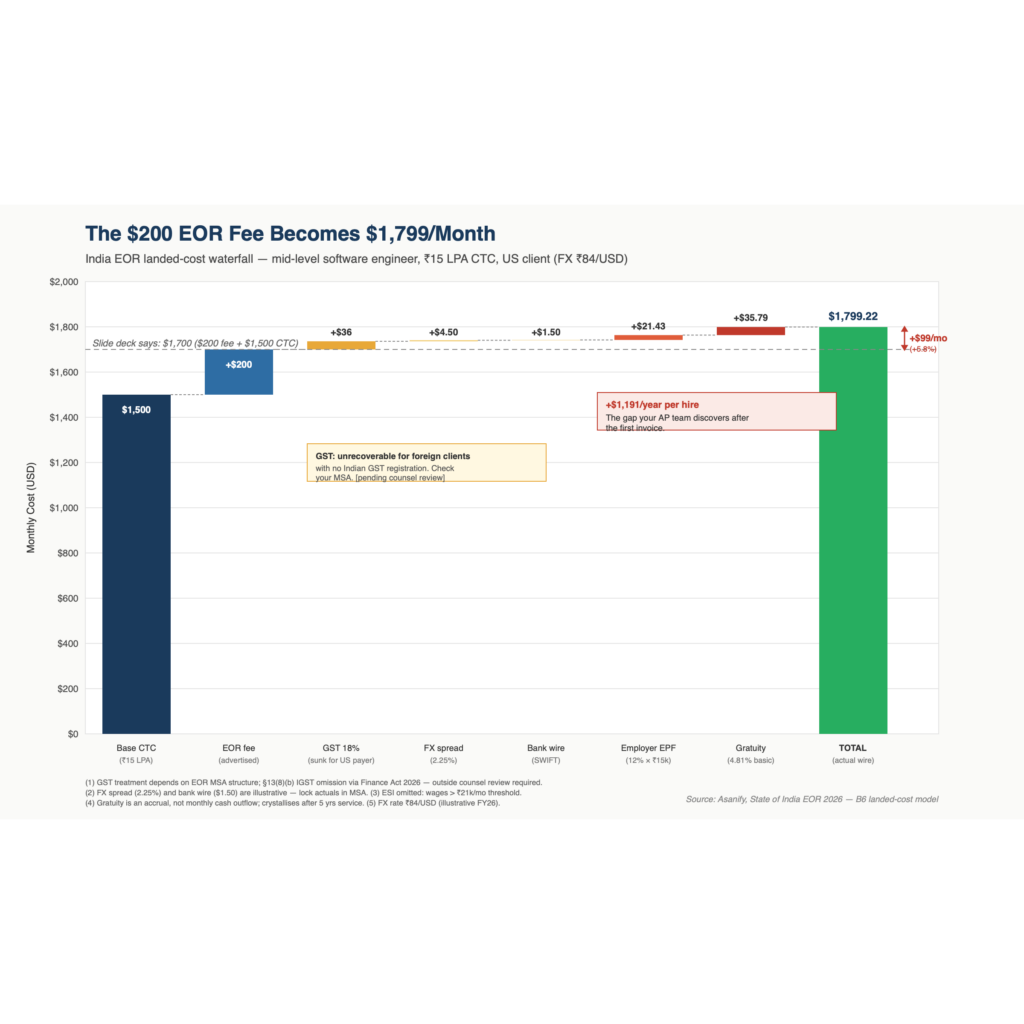

- A $1,700/month India EOR quote becomes ~$1,800/month in actual landed cost — a $98/month gap per employee. A $1,500 CTC hire plus a $200 EOR management fee looks like $1,700 on paper, but employer EPF, gratuity provisioning, GST exposure, FX markup, and bank charges push the real monthly cost to about $1,800. CFOs should model landed cost, not salary plus management fee. (Source: Section B6 — What India EOR Actually Costs.)

Executive Summary

India is not the back-office hire it was a decade ago. For companies in the US, UK, EMEA, and APAC, it is now one of the most serious places to build engineering, product, finance, operations, and customer teams. Deep talent, a cost gap that still matters in 2026, and English-language operating maturity across most of the urban hiring base.

That is why EOR adoption in India is accelerating.

What surprised us is who is adopting it. The popular image is a 500-person US tech company executing a planned India expansion. That is not what our data shows. In our closed-engagement cohort the median global headcount at sign-on is around 50, with the 25th percentile at 14 (n=22 closed-won India EOR engagements, April 2023 to April 2026). EOR has quickly become a market-entry operating model for companies in their first year of international hiring.

That is good news. A 50-person company can now hire engineers in Bengaluru without first opening an entity, hiring a local payroll team, or putting a finance controller on the ground.

Fast is not the same as informal.

Six tribunal rulings and one Supreme Court bench between July 2025 and March 2026 meaningfully changed the test for when a foreign company’s India hires create a taxable presence. An engineer building internal product is a very different risk profile from a sales leader negotiating customer terms. Whether your India contractor’s code actually belongs to you turns on a Section 19 (of the Copyright Act 1957)-compliant assignment most US-style boilerplate fails. And the quoted monthly EOR cost is rarely the total cost: a $1,500 CTC engineer with a $200 management fee costs closer to $1,800 once employer EPF, gratuity provisioning, and the FX spread are added.

From the report, in short:

- EOR provides strong value but is not a blanket permanent establishment shield. What the hire does in India matters more than whose payroll they sit on.

- India cost savings are material. CFOs should model landed cost, not salary plus management fee.

- Contractor misclassification risk is high when the working relationship looks like employment.

- Equity grants need India-specific tax and FEMA planning before the grant, not at exercise.

- The “switch to entity at 25 employees” rule of thumb is surprisingly outdated. The crossover can possibly be at 50+ hires under the posture Indian counsel typically recommend.

In our view: India is absolutely worth hiring in. EOR is often the cleanest way to begin, and the best companies will use it deliberately, with clear visibility on role-level exposure and a line of sight to when the entity math actually flips.

This report is written for that company.

🗺️ WHERE TO START — FIND YOUR SECTION IN 30 SECONDS

Currently using contractors in India? → Read B4 immediately. The EPFO amnesty that let companies regularise misclassified workers cheaply closed April 30, 2026. The enforcement window is now open.

Hiring engineers or developers through EOR? → B3 (you may not own the IP you think you own), then B7 (your payroll structure may need updating as Labour Codes roll out state by state).

Hiring salespeople, country managers, or anyone customer-facing? → B1 is your most urgent read. The EOR wrapper does not protect you from Indian tax on your company’s profits if the wrong person is doing the wrong job in India.

Evaluating EOR cost before signing a contract? → B6 (the true landed cost), then B9 (when your own India entity becomes cheaper than EOR).

Planning equity grants for your India team? → B5. The cash-flow implications at exercise are material and cannot be restructured after the grant.

About to let someone go in India? → B8. India is not at-will. The exit cost waterfall is significantly larger than most US and European companies budget for.

This report covers nine India-specific risks and decisions:

- B1 — PE risk and the 2025–2026 ruling record (six tribunals, one Supreme Court bench)

- B2 — Moonlighting, dual employment, and the UAN detection mechanism

- B3 — IP assignment chain and the contractor copyright trap

- B4 — EPF/ESI misclassification and the EPFO amnesty that closed April 30, 2026

- B5 — ESOPs and equity for India EOR employees: the cash-flow trap at exercise

- B6 — GST structure, the full landed-cost waterfall, and what $200/month actually costs

- B7 — Labour Code state notification tracker: one law, 36 implementation schedules

- B8 — Termination cost waterfall, the 4-year-240-day gratuity rule, 2-day F&F settlement

- B9 — The three-scenario EOR-vs-entity crossover model: 2, 22, or 52 India-side employees (57 including US-side accounting overhead)

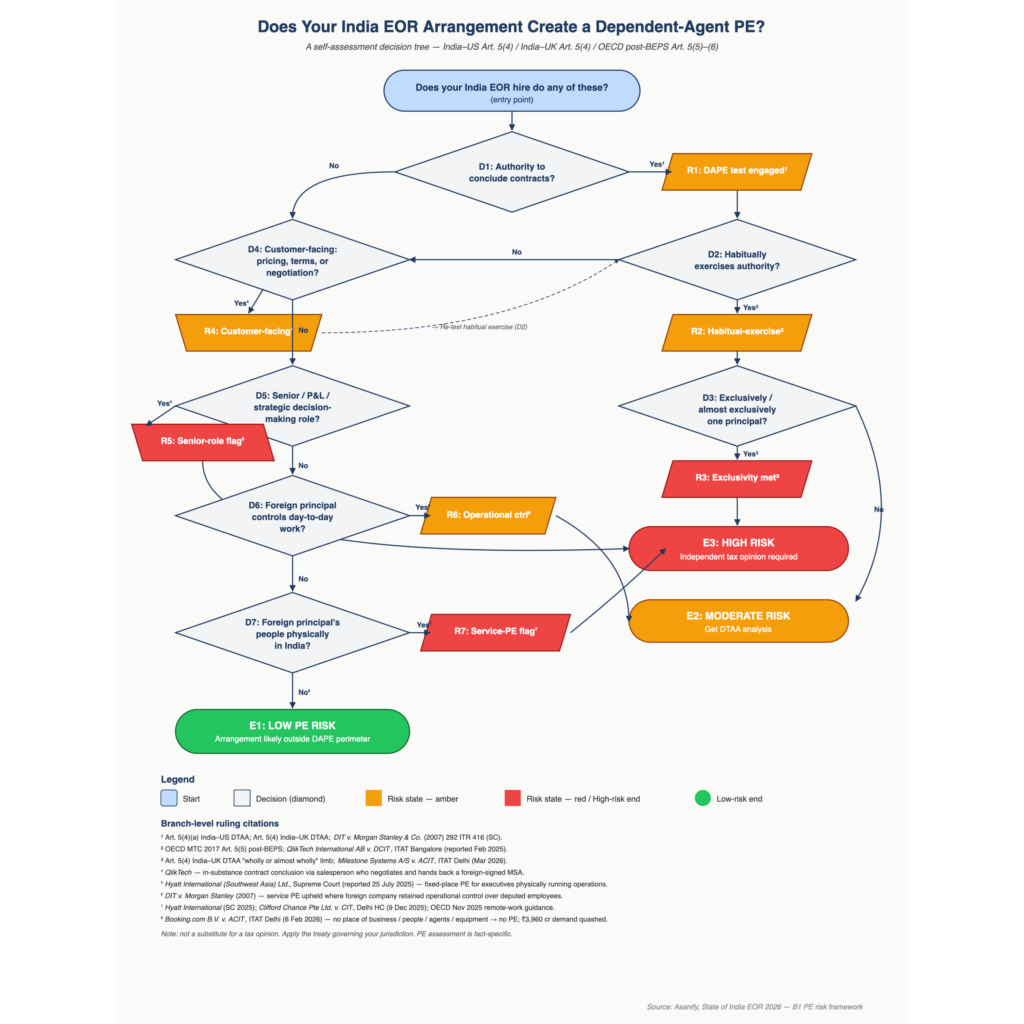

B1. Permanent Establishment: How Foreign EOR Users Stay on the Protected Side

Figure D1 — Permanent Establishment risk decision flowchart for India EOR engagements.

TL;DR — B1: The EOR wrapper does not automatically shield your company from Indian tax on its profits. What matters is what your India employees do. Six court rulings in 18 months have tightened the test. Engineers building internal product are generally safe. Salespeople with customer authority, and country managers running local P&L, are generally not. Three questions at the end of this section tell you what to ask your EOR provider. The work is in the role design at onboarding and the engagement documentation that follows. The four-test framework below is the lens Asanify uses to flag exposure with clients before it crystallises.

Between July 2025 and March 2026, six Indian tribunals and one Supreme Court bench handed down PE rulings that, taken together, redrew the line between a safe foreign-principal-with-Indian-help arrangement and a taxable permanent establishment. The headline numbers are not subtle. The Delhi ITAT, in February 2026, set aside a ₹3,960 crore demand against Booking.com B.V. on the finding that the platform’s third-party Indian hotels did not constitute a PE under Article 5 of the India–Netherlands DTAA (Taxscan). Five months earlier, the Supreme Court went the other way on Hyatt International, ruling that “even in the absence of an exclusive lease or physical office, the continuous and systematic use of another entity’s premises” can create a fixed-place PE (Worklaw; underlying Delhi HC Full Bench at Indian Kanoon doc 124906522). Both rulings sit on the same factual axis a US Head of Global Expansion now confronts: when does an Indian person doing work for a foreign company become, in tax-law terms, that foreign company?

The Indian EOR market answered the same question in marketing copy for years — “EOR shields you from PE.” That answer was always too clean. The 2025–2026 record makes the question worth a re-read.

🗺️ NEW TO PERMANENT ESTABLISHMENT? START HERE.

A “permanent establishment” (PE) is the legal trigger that allows India to tax your company’s business profits — not just your Indian employees’ salaries. If the Indian tax authority finds a PE, it can assess tax on the profits your entire company earned from its Indian operations. This is a corporate income tax exposure, not a payroll issue.

The EOR does not automatically prevent this. Whether your India hires trigger PE exposure depends on what they do — whether they negotiate contracts, interact with Indian customers, or make pricing decisions — not on whose payroll they sit. The six rulings covered in this section show exactly where the line now sits.

The Article 5 hook, and why it matters for EORs

Permanent establishment is the trigger under every Indian DTAA for taxing a foreign enterprise’s business profits in India.

The Article 5 trigger most relevant to EOR arrangements is the dependent-agent PE (DAPE). The Supreme Court in DIT v. Morgan Stanley & Co. (2007) 292 ITR 416 SC summarised the Article 5(4) test: “an assessee shall be deemed to have a permanent establishment if, inter alia, a person other than an agent of an independent status habitually exercises an authority to conclude contracts on behalf of the assessee.”

The parallel India–UK clause — broader on its face — catches an agent who “has, and habitually exercises in that State, an authority to negotiate and enter into contracts for or on behalf of the enterprise” and extends to one who “habitually secures orders in the first-mentioned State, wholly or almost wholly for the enterprise itself” (Article 5(4), India–UK DTAA, 1993 Convention as amended by the 2013 Protocol and 2020 Synthesised Text with the MLI; UK HMRC-hosted treaty text at assets.publishing.service.gov.uk PDF). Same backbone. Both texts ask one question: is the Indian-side person concluding (or playing the principal role leading to) contracts the foreign enterprise is bound by.

The OECD’s post-BEPS commentary on Article 5(5) — the model the MLI imports into India’s treaty network — sharpens it further: a DAPE arises where a person “habitually concludes contracts, or habitually plays the principal role leading to the conclusion of contracts that are routinely concluded without material modification by the enterprise” (OECD MTC 2017 Commentary, condensed; language originated in the OECD BEPS Action 7 Final Report 2015).

The risk for an EOR arrangement is not that the EOR’s payroll administrator concludes contracts. The risk is the engineer or country manager whose salary the EOR pays. If that engineer is in substance taking pricing decisions, signing SOWs, or closing customers on behalf of the foreign principal, the EOR wrapper does not change the tax answer.

What 2025–2026 actually said (six rulings, one direction with caveats)

| # | Ruling | Court / Date | Treaty | Outcome | Operative test |

|---|---|---|---|---|---|

| 1 | QlikTech International AB v. DCIT, IT(IT)A No. 990/Bang/2023 | ITAT Bangalore, 16 Dec 2024 (reported Feb 2025) | India–Sweden | DAPE attribution set aside; remanded | Arm’s-length TP adjustment extinguishes separate DAPE attribution (Taxscan) |

| 2 | RGA International Reinsurance Co. v. DCIT | ITAT Mumbai, July 2025 | India–Ireland | No DAPE, no Fixed-Place PE | Anti-fragmentation rule (India–Ireland DTAA, MLI-modified) bites only where activities are “complementary…cohesive business operation” (KPMG TaxNewsFlash) |

| 3 | Hyatt International (Southwest Asia) Ltd. | Supreme Court, reported 25 July 2025 | India–UAE | PE upheld (Fixed Place) | “Continuous and systematic use” of another’s premises = Fixed-Place PE (Worklaw; underlying Delhi HC Full Bench at Indian Kanoon doc 124906522) |

| 4 | CIT v. Clifford Chance Pte Ltd. | Delhi HC, 9 Dec 2025 | India–Singapore | No Service PE | “Physical presence of employees in India providing services to clients is a precondition for the constitution of service PE” (KPMG TaxNewsFlash) |

| 5 | Booking.com B.V. v. ACIT, ITA No. 2033/Del/2025 | ITAT Delhi, 6 Feb 2026 | India–Netherlands | No Fixed-Place / No Agency PE; ₹3,960 crore demand quashed | Foreign platform with no place of business, personnel, agents, or equipment in India is not a PE (Taxscan) |

| 6 | Milestone Systems A/S v. ACIT, AY 2022-23 | ITAT Delhi, March 2026 | India–Denmark | No DAPE | Principal-to-principal distributor, bearing its own risk and free of detailed instructions, is not an agent (The Tax Corp) |

Five rulings narrowed PE; the sixth — Hyatt at the Supreme Court — widened it. Read the loss carefully. Hyatt’s executives were physically in India, repeatedly, running the hotel — exactly the fact pattern a US engineering VP creates when they fly to Bengaluru monthly to “run sprints with the team.” The dominant 2025–2026 thread is that tribunals are tightening the DAPE test: real legal and economic dependence, habitual contract conclusion, no preparatory/auxiliary carve-out abuse. The contra-thread is service PE through people who actually show up.

The four threshold tests, in the order an Assessing Officer might run them

The way an AO builds a PE case against a foreign EOR user — distilled from the six rulings above and the Morgan Stanley “lien on payroll” framework — is sequential. If the EOR arrangement passes all four, the structure holds. If it fails one, the rest do not save it.

-

Day-to-day control of the worker. Who sets the daily work, conducts performance reviews, and decides promotions? Morgan Stanley upheld a service PE precisely where the foreign company retained operational control and the deputed employees stayed on its payroll/lien. EOR arrangements where the foreign principal directly manages day-to-day output are functionally indistinguishable.

-

Customer-facing authority. Does the India-resident person interact with the foreign company’s customers — pricing, negotiation, scope, terms? QlikTech‘s Indian subsidiary did all three (customer identification, price negotiation, contract finalization), and the AO’s DAPE attribution only got knocked down because TP had already taxed the same flow. Milestone Systems survived because the Indian distributor stood on its own as principal.

-

Contract-signing authority — formal or in-substance. The India–US treaty wording requires habitually “exercising an authority to conclude contracts.” The OECD MTC post-BEPS test extends this to “habitually plays the principal role leading to the conclusion of contracts that are routinely concluded without material modification.” A salesperson who hands a US-signed MSA back to the customer with negotiated commercial terms qualifies even though the ink is American.

-

Economic substance and risk-bearing. Booking.com survived because no Booking-employed person, no Booking equipment, and no Booking place of business sat in India. Hyatt failed because Hyatt’s people and operational control did. Morgan Stanley settled the corollary: once an Indian affiliate is compensated at arm’s length for its functions, “no further profits would be attributable” (Indian Kanoon doc 584977) — but this defence presupposes that the Indian-side risk and reward genuinely sit with the Indian entity, not back-loaded onto the foreign parent.

PE risk at onboarding. Evaluating PE exposure is the foreign principal’s responsibility. Asanify’s clients who want a written role profile can request an engagement risk note before onboarding. The note checks the role against the four operational PE factors and flags it low-risk, attention-needed, or refer-to-counsel. It is operational triage, not a tax or legal opinion, and does not relieve the client of its own analysis.

EOR-protected vs EOR-vulnerable arrangements

The same fact pattern that creates exposure in one role can be designed out of exposure in a different role. The table sets out where each common India EOR role sits today on the dependent-agent PE axis. Asanify works with foreign principals at onboarding to keep roles on the protected side wherever the role design permits.

| Arrangement | Likely PE position | Why |

|---|---|---|

| EOR engineer building product the foreign principal sells globally, code committed to the foreign company’s repo, no Indian customer contact | EOR-protected | No customer-facing authority, no contracts concluded in India; the work is internal-facing R&D analogous to Morgan Stanley back-office (preparatory/auxiliary on a good day; arm’s-length TP if questioned) |

| EOR sales rep with a quota, Indian customer book, and authority to negotiate terms | EOR-vulnerable | Hits Article 5(4) clause (a) of the India–UK DTAA verbatim — “habitually exercises…an authority to negotiate and enter into contracts” — even if final signature is in San Francisco |

| EOR country manager who flies to client sites, signs LOIs, and runs the India P&L for the foreign principal | EOR-vulnerable | Triple-hit: dependent-agent role, customer-facing authority, and (per Hyatt) continuous and systematic presence at premises that are not the EOR’s |

| EOR customer-support engineer handling Indian customers of a foreign SaaS product | Grey | Depends on whether the foreign principal also has any physical presence; Clifford Chance‘s rule — no physical presence, no service PE — protects if the foreign company itself never sends people |

| Foreign-company VP who relocates to India “for personal reasons” and continues running their global team | EOR-vulnerable | OECD November 2025 remote-work guidance flags that sustained working hours at a non-employer location, when paired with a genuine commercial reason (e.g., serving local clients), can crystallise a place of business (KPMG SE summary |

Three questions to align with your EOR provider on PE Risk

-

Authority and role design. Who is responsible for ensuring your India hires’ customer-facing authority stays within the four-factor PE-safe zone, your engagement documentation, the EOR’s contract templates, or both? What does the answer mean for hires in sales or country-management roles where contract-conclusion authority is part of the job?

-

Indemnity allocation. How does your EOR provider allocate PE risk in the MSA, indemnity scope, per-engagement or per-employee cap, and client-conduct carve-outs, and how does that allocation compare to your realistic attributed-profits exposure on the role mix you plan to hire?

-

Service-PE day-counting. If your foreign-resident employees travel to India regularly, how is the engagement set up to support service-PE day-counting evidence under the common-day rule applied in Clifford Chance, through your own travel records, through your EOR’s logs, or by a documented protocol between you?

The 2025–2026 case law gives a foreign EOR user more cover than the pre-2025 secondment jurisprudence suggested. Where the facts look like Hyatt’s, no employment structure changes the answer. Where the facts look like Booking.com’s or Milestone’s, the structure does not have to fail. The four-factor test is where the work happens.

The work is in the role design and the documented engagement. Foreign principals who treat PE exposure as a continuous design problem, not a one-time onboarding check, are the ones the post-2025 record consistently treats favourably.

B2. Moonlighting and Dual Employment Under Indian Law

TL;DR — B2: India has no law against moonlighting — but your EOR employment contract can prohibit it, and Indian courts will enforce that prohibition during employment. The risk for foreign companies is threefold: IP leakage if the engineer is building a competing product, EPF compliance exceptions when dual contributions surface, and a weak termination case if the contract was generic. Moonlighting risk is best managed through a combination of pre-hire verification, in-service exclusivity in the employment contract, and ongoing visibility into the worker’s EPFO record. The operational mix and cadence vary by provider.

On 21 September 2022, Wipro’s then-Chairman Rishad Premji publicly stated that “there is no space for someone to work for Wipro and competitor XYZ” and that “I do think it is violation of integrity if you are moonlighting in that shape and form” (TechCrunch, Manish Singh, 21 September 2022). Wipro had just terminated 300 Indian employees discovered drawing a second paycheque while on Wipro’s rolls. Within ninety days, every tier-1 Indian IT services company had taken a public position on dual employment, and three years later the question still sits on the desk of every foreign engineering leader hiring through an Indian EOR. India never passed a statute against moonlighting. It did not need to. The risk lives in the contract, the EPF UAN, and the model standing orders — and a foreign employer hiring through an EOR inherits all three.

The 2022–2025 timeline, in the IT majors’ own words

Wipro (September 2022). Per the same TechCrunch dispatch: “Wipro terminated 300 of its Indian staff members on grounds that they had obtained secondary employment without consent.” Premji’s distinction was specific — “individuals can have candid and open conversations around playing in a band or working on a project over the weekend,” but a parallel role at a competitor was, in his framing, an integrity breach.

Infosys (September 2022, then reversed). The original Infosys appointment letter language read: “Employees agree not to undertake employment, whether full-time or part-time, as director/partner/member/employee of any other organization engaged in any form of business activity without the consent of Infosys, and consent may be withdrawn at any time at the discretion of the company” (Business Today, 30 August 2022). Within weeks the company reversed: Infosys emailed staff that “Any employee, who wishes to take up gig work, may do so, with the prior consent of their manager and BP-HR, and in their personal time, for establishments that do not compete with Infosys or Infosys’ clients” (Business Today, Tarab Zaidi, 20 October 2022). CEO Salil Parekh later confirmed on a Q2 earnings call that Infosys had terminated employees who moonlighted in the preceding twelve months.

TCS (September 2022). TCS’s appointment letter clause is the strictest of the four: “Either during the period of your traineeship or during the period of your employment as a confirmed employee of TCSL, you are not permitted to undertake any other employment, business, assume any public or private office, honorary or remunerative, without the prior written permission of TCSL” (Business Today, 30 August 2022). COO N. Ganapathy Subramaniam framed it publicly as an “ethical issue.”

Tech Mahindra and HCL Tech. All five — TCS, Infosys, Wipro, Tech Mahindra, and HCL Tech — carry appointment-letter clauses that prohibit secondary employment without consent (Business Today, 30 August 2022, as above). NASSCOM President Debjani Ghosh’s September 2022 framing was the industry’s diplomatic middle: “The problem happens when you are a full time worker and you decide to pursue other opportunities without informing your current employer about your decision. That’s where the trust between employer and employees breaks down” (Business Standard, 22 September 2022).

By 2025, the policy direction had split: punitive enforcement at the tier-1 IT majors; permissive carve-outs in the central government’s draft Model Standing Orders under the Occupational Safety, Health and Working Conditions Code 2020, which contemplate allowing “ethical moonlighting” provided employees obtain prior permission from their primary employer (Business Standard / NASSCOM, 22 September 2022).

What the statute actually says (and does not say)

“Indian laws are silent on moonlighting, and there is no explicit legal prohibition against holding multiple jobs” (Lexology synthesis). There is no section of any Act that says “do not work two jobs.” What exists instead is a four-layer scaffold that, taken together, gives an employer a credible termination case — if the employer drafted the contract correctly.

Layer 1 — Common-law duty of fidelity. An employee owes the employer a duty of good faith in performance of the employment contract. Indian courts have recognized this principle — consistent with English common-law doctrine — in the employment context. In Niranjan Shankar Golikari v. The Century Spinning and Mfg. Co. Ltd. (1967 AIR 1098), the Supreme Court held that negative covenants during the period of employment do not constitute a restraint of trade under Section 27 of the Indian Contract Act, affirming that in-service fidelity obligations are valid and enforceable. The Supreme Court in Manager, Pyarchand Kesarimal Ponwal Bidi Factory v. Omkar Laxman Thange and Ors. (AIR 1970 SC 823) further established that a subsisting contract of service with one employer is a bar to concurrent service with another, unless the contract provides otherwise or the primary employer consents (Cyril Amarchand Mangaldas, October 2022). This is the doctrinal anchor most often cited in moonlighting termination letters from tier-1 IT firms.

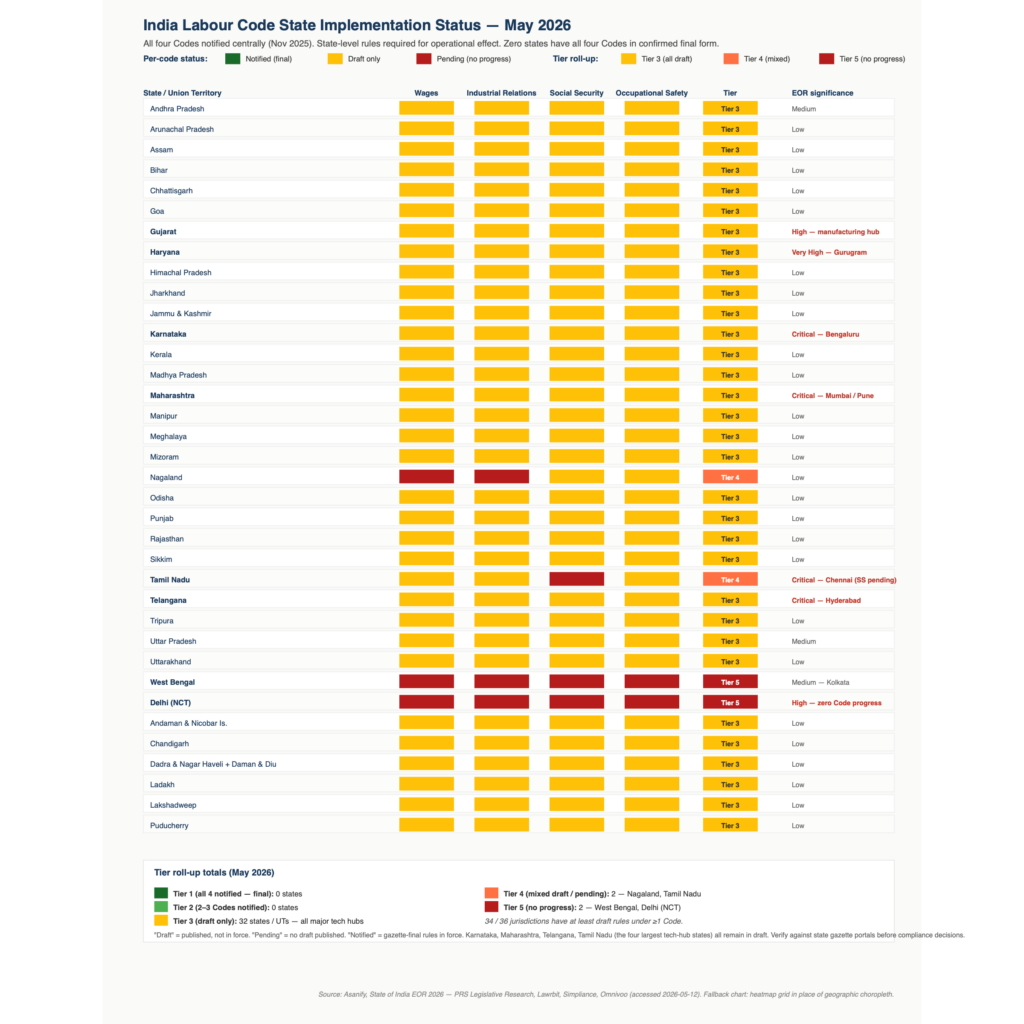

Layer 2 — Industrial Employment (Standing Orders) Act 1946, now subsumed by the Industrial Relations Code 2020. Schedule I of the Model Standing Orders has historically listed “habitual absence” and conduct prejudicial to the employer’s interest as misconduct grounds. Under the IR Code 2020 (consolidation effective 21 November 2025), the Model Standing Orders carry forward the misconduct framework, with a draft ethical-moonlighting carve-out described above (PRS Legislative Research — Labour Law Reforms Overview).

Layer 3 — Section 60, Factories Act 1948. The provision reads: “No adult worker shall be required or allowed to work in any factory on any day on which he has already been working in any other factory, save in such circumstances as may be prescribed” (IndiaKanoon, Section 60, Factories Act 1948). This is narrow — it covers factory workers, not software engineers — but it is the only piece of central legislation that directly bars dual employment, and it is the citation most commonly mistaken for a general rule.

Layer 4 — State Shops & Establishments Acts. State law varies. The Maharashtra Shops and Establishments (Regulation of Employment and Conditions of Service) Act 2017 restricts an employee from working in any establishment on a day on which the employee is on holiday or leave under that Act — a holiday-day curb, not a general dual-employment bar (India Code — Maharashtra Shops and Establishments Act 2017). Karnataka’s Shops and Commercial Establishments Act 1961 is structured similarly — the operative restriction on working hours sits outside a dedicated dual-employment section.

The non-compete trap. Section 27 of the Indian Contract Act 1872 voids agreements in restraint of trade. Indian courts have read this strictly during the term of employment — an in-service duty-of-fidelity restraint is enforceable (Niranjan Shankar Golikari, above) — and even more strictly after termination, where post-employment non-competes are largely unenforceable except on sale of goodwill. A foreign employer accustomed to Californian non-compete jurisprudence inverts the risk: the in-service restraint is usable; the post-exit clause is paper.

What this means for a foreign company hiring via an Indian EOR

The EOR is the legal employer. The contract the engineer signs is the EOR’s contract — not the foreign principal’s. If that contract is generic (a Word-template “employee agreement” the EOR uses for every client), three things break.

Dual-employment exposure on the EOR’s books. The Indian engineer is on the EOR’s payroll. If she also draws a salary from another Indian employer, both companies file EPF contributions against her single Universal Account Number. The EPFO’s UAN consolidation makes the dual contribution visible in payroll reports the moment the second employer files its first ECR. Reporting at the time — including Outlook Business — theorized that Wipro identified the 300 cases through EPF UAN cross-reference, when a second employer’s ECR filings surfaced against the same UAN. The foreign principal does not see this; the EOR does. Whether the EOR tells the principal depends on the SLA.

ESI and PF complications. A single employee with two PF accruals at once creates a payroll exception that ESIC and EPFO routinely flag. The penalty risk sits with the EOR as legal employer; the indemnity sits in the MSA the foreign principal signed.

IP-leakage risk. This is the operative concern, and it cross-references to B3. Indian copyright assignment requires a written instrument (Section 19, Copyright Act 1957); employer ownership of works made in the course of employment under Section 17(c) attaches only to the legal employer — which is the EOR. If the engineer is moonlighting on a competing product, the foreign principal’s contractual claim against the engineer is mediated through the EOR’s agreement. A weak EOR contract is a weak IP fence.

What a competent EOR actually does

A mature moonlighting program for an India EOR engagement combines three elements. First, pre-hire background verification that surfaces existing employment, ideally including EPF UAN history. Second, ongoing visibility into the EPFO record so dual-contribution signals can be flagged when they appear. Third, a confidentiality and exclusivity clause in the employment contract that specifies prior written consent for any secondary engagement, making termination defensible on contractual grounds, not on the unstable footing of an implied duty. The maturity and cadence of each element varies materially across providers.

Two operational mechanisms separate India-specialist EORs from generalist platforms on this dimension: (a) whether the EOR runs an active UAN cross-reference job against EPFO records each payroll cycle, and (b) whether the employment-agreement template names secondary employment as a Schedule-I-misconduct ground under the IR Code 2020 Model Standing Orders. The right diligence question is: “show me the exception report and the clause.” If the provider cannot produce both in writing, the moonlighting fence is paper. For an engineer building production code, that gap is where the IP claim leaks.

Moonlighting at onboarding and during employment. Asanify’s standard India employment agreement includes exclusivity and in-service restraint language enforceable under Section 27 of the Indian Contract Act 1872 (Niranjan Shankar Golikari v. The Century Spinning and Mfg. Co. Ltd., 1967 AIR 1098). Pre-hire background verification flags previously declared employment. Foreign principals concerned about dual-employment exposure on a specific hire can request a UAN-level employment-status check before onboarding.

Five contract clauses that India-specialist EORs should ideally include — and what each one does

- Exclusivity with consent carve-out. “Employee shall not engage in any other employment, consultancy, or business activity, paid or unpaid, without the prior written consent of the Employer, which consent shall not be unreasonably withheld for activities that do not compete with the Client’s business or impair the Employee’s duties.” Tracks the Infosys post-September-2022 model, not the pre-September Wipro absolutism.

- Confidentiality covering Client-derived information with explicit reference to Section 17(c) Copyright Act 1957 work-for-hire vesting and Section 19 written-assignment formalities — so the EOR holds and assigns the IP to the foreign principal cleanly.

- Section 27 ICA-compliant in-service restraint — enforceable during employment per Niranjan Shankar Golikari (1967 AIR 1098) — paired with a narrow, time-limited post-employment confidentiality covenant (not a post-employment non-compete, which Indian courts will not enforce).

- EPF UAN and PAN disclosure obligation at onboarding and on a quarterly affirmation, with a contractual right for the EOR to query EPFO records — turning UAN cross-reference from a forensic tool into a routine compliance check.

- Termination for misconduct aligned with Model Standing Orders under IR Code 2020 Schedule I — naming undisclosed secondary employment as misconduct. For non-workmen (the category most foreign-EOR technology hires fall into under the Industrial Disputes Act 1947 §2(s)), termination for proved misconduct proceeds without notice pay or retrenchment compensation. For workmen, a domestic inquiry establishing the misconduct is required before that outcome is available (AZB & Partners — Employment Termination in India, 22 September 2025).

These clauses are descriptive of best practice for an India-specialist EOR’s employment contract. They are not legal advice.

Three questions to align with your EOR provider on moonlighting

-

Contract design. Does the EOR’s standard India employment contract include an exclusivity clause with prior-written-consent? Where the absolutist version is in use, what is the operational practice for granting consent to non-competing side engagements like teaching, writing, or open-source contribution?

-

Detection cadence. What is the EOR’s standing process for surfacing dual-contribution signals from the EPFO portal, and how does that cadence compare to the rate at which signals typically appear for your engagement size?

-

Termination defensibility. If a moonlighting situation surfaces, what is the EOR’s standard documentation chain (charge-sheet, response opportunity, inquiry record) that would survive a labour-tribunal challenge for a workman-classified hire?

B3. IP Assignment Under Indian Law: The Contractor Leakage Trap

TL;DR — B3: Indian copyright law defaults to author ownership, not employer ownership. The employer exception only applies to employees under a “contract of service” — not to contractors. If your India team was engaged as contractors, they own the IP until a valid written assignment transfers it. That assignment must address four specific legal requirements where US-style “all IP hereby assigned” clauses are commonly under-specified. EOR fixes the employment status problem — but the EOR still needs to hold a Section 19-aligned assignment from the employee, and your company needs a back-to-back assignment from the EOR.

⚠️ THE IP CHAIN PROBLEM — HERE IS THE TRAP IN FIVE STEPS

- A US company hires “three contractors in Bengaluru” through a global platform.

- The contract has a standard US-style clause: “All IP created under this agreement is hereby assigned to the company.”

- The contractors build the product — code, ML model weights, the customer onboarding playbook.

- Two years later, the company starts a fundraising round. The investor’s counsel asks for the chain of IP title.

- There is no valid chain. Under Indian copyright law, the contractors own the code — because (a) they were not employees under a “contract of service,” so the employer-vesting rule never applied; and (b) the US-style assignment clause fails Indian law’s specificity requirements on at least four grounds.

EOR conversion fixes step 1. The rest of the chain is where the work happens. Copyright vests in the EOR entity — the legal employer — not in your company. Your company still needs a Section 19-aligned written assignment from the EOR. If the EOR’s employment agreement relies on a generic “all IP” clause without the Section 19 specificity, the chain has gaps your IP counsel will want to inspect.

The single most expensive mistake a foreign company makes when hiring in India is treating the country like a US-style “work for hire” jurisdiction. It isn’t. Indian copyright’s default rule is author-first ownership — and the employer exception that matters for your India hire does not apply to contractors. If your Bengaluru engineers have been on a contractor arrangement through a global platform, they own the code until a Section 19-compliant written assignment moves it. Section 17’s employer-vesting exception only fires when the work is made “in the course of the author’s employment under a contract of service or apprenticeship.” Contractors are not under a contract of service. That gap is the leakage mechanism.

This is not a theoretical wrinkle. It is the structural reason why a tier-1 US acquirer’s IP-diligence checklist will torch a deal where the India team was on a “contractor” arrangement and never went through the formality of a signed, work-identified, rights-enumerated assignment. The acquirer’s counsel knows what to ask. Most India hiring stacks were not built to answer.

What the statute actually says

Section 17, Copyright Act 1957 — First owner of copyright. “Subject to the provisions of this Act, the author of a work shall be the first owner of the copyright therein.” That is the default rule. The exceptions are the operative provisions for hiring:

- Proviso (b) — commissioned works: “In the case of a photograph taken, or a painting or portrait drawn, or an engraving or a cinematograph film made, for valuable consideration at the instance of any person, such person shall, in the absence of any agreement to the contrary, be the first owner of the copyright.” (Indian Kanoon doc 1404402.)

- Proviso (c) — employment: Where a work is made “in the course of the author’s employment under a contract of service or apprenticeship,” the employer is the first owner of copyright in the work — subject to any agreement to the contrary. (Indian Kanoon doc 1404402.)

The default (author owns) and the exception (employer owns works created in the course of employment under a contract of service) carry two consequences that matter for the EOR fact pattern:

First, where an EOR arrangement is in place, the EOR entity is the employer of record under the contract of service — so copyright vests in the EOR entity, not in the foreign client. The foreign client is a third party who must receive an explicit assignment from the EOR to hold title.

Second, where workers are classified as contractors (not employed under a contract of service), proviso (c) does not apply at all. The contractors retain first ownership of everything they create until a compliant assignment transfers it.

Note what proviso (b) does not cover: software, ML model weights, training datasets, sales playbooks, technical drawings. The commissioned-works exception is limited to photographs, paintings, engravings, and films. A contractor building a product is not producing any of these. That contractor retains first ownership.

Section 19, Copyright Act 1957 — Mode of assignment. (Indian Kanoon doc 262036; verbatim.)

Section 19(1): “No assignment of the copyright in any work shall be valid unless it is in writing signed by the assignor or by his duly authorised agent.”

Section 19(2): “The assignment of copyright in any work shall identify such work, and shall specify the rights assigned and the duration and territorial extent of such assignment.”

Section 19(3): “The assignment of copyright in any work shall also specify the amount of royalty and any other consideration payable, to the author or his legal heirs during the currency of the assignment and the assignment shall be subject to revision, extension or termination on terms mutually agreed upon by the parties.”

The three operative default rules that create the most practical risk:

- §19(4) — one-year lapse: “Where the assignee does not exercise the right assigned to him under any of the other sub-sections of this section within period of one year from the date of assignment, the assignment in respect of such rights shall be deemed to have lapsed after the expiry of the said period unless otherwise specified in the assignment.” (Indian Kanoon doc 34094353; verbatim.)

- §19(5) — five-year default duration: “If the period of assignment is not stated, it shall be deemed to be five years from the date of assignment.”

- §19(6) — India-only territorial default: “If the territorial extent of assignment of the rights is not specified, it shall be presumed to extend within India.”

Section 19(7) — Pre-1994 assignments. Section 19(7) provides: “Nothing in sub-section (2) or sub-section (3) or sub-section (4) or sub-section (5) or sub-section (6) shall be applicable to assignments made before the coming into force of the Copyright (Amendment) Act, 1994.” (Indian Kanoon doc 262036; verbatim.) For any post-1994 assignment — which covers every contemporary EOR arrangement — all five specificity requirements (§§19(2)–19(6)) are in full force.

Note on future copyright: the statutory mechanism for capturing works yet to come into existence is operative through §§19(2)–(3) read with standard Indian contractual drafting practice (the assignment identifies future categories of work by description). A well-drafted EOR employment contract that identifies work by category — “all software, ML models, technical documentation, and data created during employment” — sweeps in work created on Day 90 as well as Day 1, because the category-identification requirement of §19(2) can be satisfied prospectively. Without this forward-looking category description in the signed agreement, an onboarding assignment may not reach works created after the signing date.

A US-style “all IP arising under this agreement is hereby assigned” boilerplate fails every one of these specificity requirements: it does not identify the work, does not specify the duration, does not state the territorial extent, and does not address the royalty consideration element. Dropped into an EOR Master Services Agreement, that clause is void as a copyright assignment under Indian law.

Patents move differently — and the deadline is harder

Sections 6 and 7, Patents Act 1970. A patent application may be filed by the true and first inventor, by an assignee, or by a legal representative. Where the application is filed by an assignee, Section 7(2) requires the applicant to furnish proof of the right to make the application — either at filing or within six months under Rule 10 of the Patents Rules 2003.

Unlike copyright, the patentable invention carries no statutory employer-vesting default in India. This is a material difference from US law, where inventions made in the scope of employment generally vest in the employer by operation of law or implied trust. In India, the employer’s claim runs entirely through the employment contract — and the contract has to be specific enough to be admissible as proof of right at the Indian Patent Office.

The Delhi High Court addressed this proof-of-right standard in Nippon Steel Corporation v. The Controller of Patents, C.A.(COMM.IPD-PAT) 10/2025, where the court considered whether a deceased inventor’s employer-employee agreement and company basic regulations were sufficient proof of right for a patent application filed by the corporate assignee. The case illustrates the doctrinal point clearly regardless of final outcome: silence in the employment contract puts the patent filing at risk.

The case law that locks it in

Eastern Book Co. v. D.B. Modak, (2008) 1 SCC 1. The Supreme Court rejected the “sweat of the brow” doctrine and adopted a “modicum of creativity” standard — copyright subsists in derivative material only where it embodies the author’s skill and judgment and exhibits more than trivial creativity. (Indian Kanoon doc 1062099.) The practical implication for foreign hirers: even with a perfect assignment in place, datasets, mechanical compilations, and routine configuration files may not clear the originality threshold and may not be protectable under Indian copyright at all.

Burlington Home Shopping Pvt. Ltd. v. Rajnish Chibber, 1995 IVAD Delhi 732. Delhi High Court, R.C. Lahoti J. (Indian Kanoon doc 130087.) A former employee took the customer database to a competing mail-order business. The court held a strong prima facie case of copyright infringement and restrained the defendant from using the customer list — the database was “exclusively owned by the plaintiff.” The doctrinal anchor was Section 17(c): the employer is the first owner where the work is created in the course of employment under a contract of service.

Burlington is the case the foreign client’s IP counsel will cite if an ex-employee walks away with source code. It rests on contract-of-service status. A contractor is not under a contract of service. The injunction Burlington won would not have been available against a contractor in the absence of a Section 19-compliant assignment.

The contractor IP-leakage trap

Here is the trap, in five steps:

- A US Series-B company hires “three contractors in Bengaluru” through a global vendor.

- The contractor agreement contains a US-style “work for hire / hereby assigned” clause.

- The contractors build the product — code, ML model weights, training data, the customer-onboarding playbook.

- Two years in, the company starts a Series C round. The acquirer’s IP counsel asks for the chain-of-title.

- There isn’t one. Section 17(c) doesn’t apply because the contractors were not employees. Section 19 fails because the assignment doesn’t identify the works, doesn’t specify duration, doesn’t state territorial extent. Under the Section 19(5)–(6) defaults, anything older than five years may have lapsed; anything not exercised within a year of assignment has lapsed unless the agreement provides otherwise.

EOR conversion fixes step 1. Section 17(c) vests copyright in the EOR entity — the Indian employer of record — for works made during employment under a contract of service. That right vests in the EOR entity; it does not flow automatically to the foreign client. The foreign client still needs a clean back-to-back assignment from the EOR. This is where the EOR’s employment-agreement template warrants scrutiny. A foreign principal conducting IP diligence (for fundraising, M&A, or platform-acquirer review) should walk through the assignment chain with IP counsel, not assume the template works.

IP assignment chain. Asanify’s standard India employment agreement includes a comprehensive IP assignment clause that enumerates work categories across copyright, patent, design, trade-secret, and confidential-information rights. The Service Addendum carries a back-to-back assignment from Asanify to the foreign client, addressing the employee-to-EOR-to-foreign-principal chain. Foreign principals conducting IP diligence (for fundraising, M&A, or platform-acquirer review) can request copies of both clauses for their IP counsel’s evaluation against the Section 19 elements that matter for their specific fact pattern.

Not sure if your India IP chain is airtight? Asanify’s employment agreement includes a comprehensive IP assignment that enumerates work categories across copyright, patent, trade-secret, and related rights. If you have been using contractors, we will walk you through a compliant conversion. Review your IP chain with Asanify →

If the EOR template does not include a Section 19-aligned assignment from the employee to the EOR, and a back-to-back assignment from the EOR to the foreign entity, the EOR conversion addresses only part of the chain. The quality of each link is variable across providers and is a fact-specific assessment for the foreign principal’s IP counsel.

Five Section 19 elements to inspect in any India IP assignment

A Section 19-aligned assignment in an Indian employment agreement (or the back-to-back EOR-to-client deed) typically addresses five elements. Where US-style boilerplate is used in an Indian setting, three of the five are commonly under-specified:

- Identify the work. “All intellectual property created during employment” is too vague. The clause must name categories with specificity — source code, ML models and weights, training data, technical documentation, customer lists, product designs.

- Specify the rights assigned. Reproduction, adaptation, translation, communication to the public, broadcasting, commercial exploitation — each enumerated. A blanket “all rights” is litigated; an enumerated list is not.

- State the duration. Use “for the full term of copyright” or “in perpetuity, to the extent permitted by law.” If the duration is silent, Section 19(5) may render the assignment ineffective after five years.

- State the territorial extent. “Worldwide” — explicitly. Silence under Section 19(6) limits the assignment to India only.

- Address royalties, future works, and moral rights. Where the assignment is in consideration of the employee’s salary, state this expressly — the royalty obligation is satisfied, not eliminated, when the consideration is the employment itself. Add a Section 19(7) forward-looking clause covering works to be created during the employment term: rights in those works take effect when each work comes into existence. On moral rights under Section 57: Indian law on the enforceability of moral-rights waivers is unsettled. Practitioners commonly address Section 57 either by including moral rights within the broader assignment, or by acknowledging the author’s moral rights coupled with a covenant by the author not to assert them. Counsel guidance varies by fact pattern; both approaches have practitioner support.

Add to that a patents-specific proof-of-right clause — Section 7(2) of the Patents Act requires the assignee to furnish proof of right within six months of filing. The employment contract is the document the Patent Office expects to see. Make sure it says what it needs to say — and that the chain runs from employee to EOR to foreign client before filing day.

Three questions to align with your EOR provider on IP

-

Employee-to-EOR assignment. What does the EOR’s employment-agreement IP assignment clause actually say? Ask for the operative clause text and the residuary IP-rights paragraph, both. The Section 19 elements (categories enumerated, rights specified, duration stated, territorial extent stated, royalty/consideration addressed) often live across multiple clauses; the full picture matters more than any single clause read in isolation.

-

Back-to-back assignment. What does the MSA or Service Addendum say about the assignment from the EOR entity to your foreign company? Same five-element inspection. A back-to-back assignment that lapses for failure to exercise within twelve months under §19(4), or that defaults to a five-year duration under §19(5), is a different proposition from one that is express and indefinite.

-

IP diligence packet. Can the EOR provide a structured IP diligence packet on request (employment-agreement template, MSA back-to-back clause, sample assignment under a specific Service Addendum) for your IP counsel’s review before an M&A or fundraising event?

B4. The Contractor Trap: Why "Just Hire Them as a 1099" Stops Working in 2026

TL;DR — B4: Indian courts look through the contract label to the economic reality of the working relationship. A “contractor” who works exclusively for you, on your tools, at a fixed monthly fee, under your managers, is likely an employee under Indian law — regardless of what the agreement says. Misclassification creates EPF back-contribution exposure with 12% annual interest plus damages. The EPFO amnesty that let employers regularise this cheaply closed April 30, 2026.

⚠️ IS YOUR INDIA “CONTRACTOR” ACTUALLY AN EMPLOYEE? — A 60-SECOND CHECK

Answer these five questions about each India contractor your company uses:

- Do they work exclusively for your company (no other clients)?

- Does your company supply their laptop, software licences, or other tools?

- Do they receive a fixed monthly fee regardless of what deliverables they submit?

- Do they report to your internal managers, attend your standups, and have OKRs or performance reviews?

- Have they been working with you continuously for more than 12 months?

If you answered yes to 3 or more: read this section carefully. Indian courts apply an economic-reality test — the label on the contract does not decide the outcome. The relationship you just described looks like employment to an Indian tribunal.

Time-sensitive: The EPFO amnesty that let employers regularise misclassified workers at low cost closed on April 30, 2026. After that date, the statutory interest and penalty regime applies in full. The cheap exit is gone.

The EPFO’s Employees’ Enrolment Campaign 2025 — a national amnesty covering workers hired between July 2017 and October 2025 — closed on April 30, 2026. The terms were unusually lenient:

- Flat ₹100 penal damage per establishment (covering EPF, EPS, and EDLI)

- Employees’ share waived where it was never deducted

- No suo-motu compliance action against participating employers — written EPFO commitment

EPFO does not run an eight-year retroactive amnesty when misclassification is rare. The campaign’s scale is the tell: the regulator found enough mis-enrolment — contractors who should have been employees, staff onboarded without PF numbers in the 2021–22 hiring boom — to justify a national clean-up before enforcement escalated. After May 1, 2026, the cheap exit is gone.

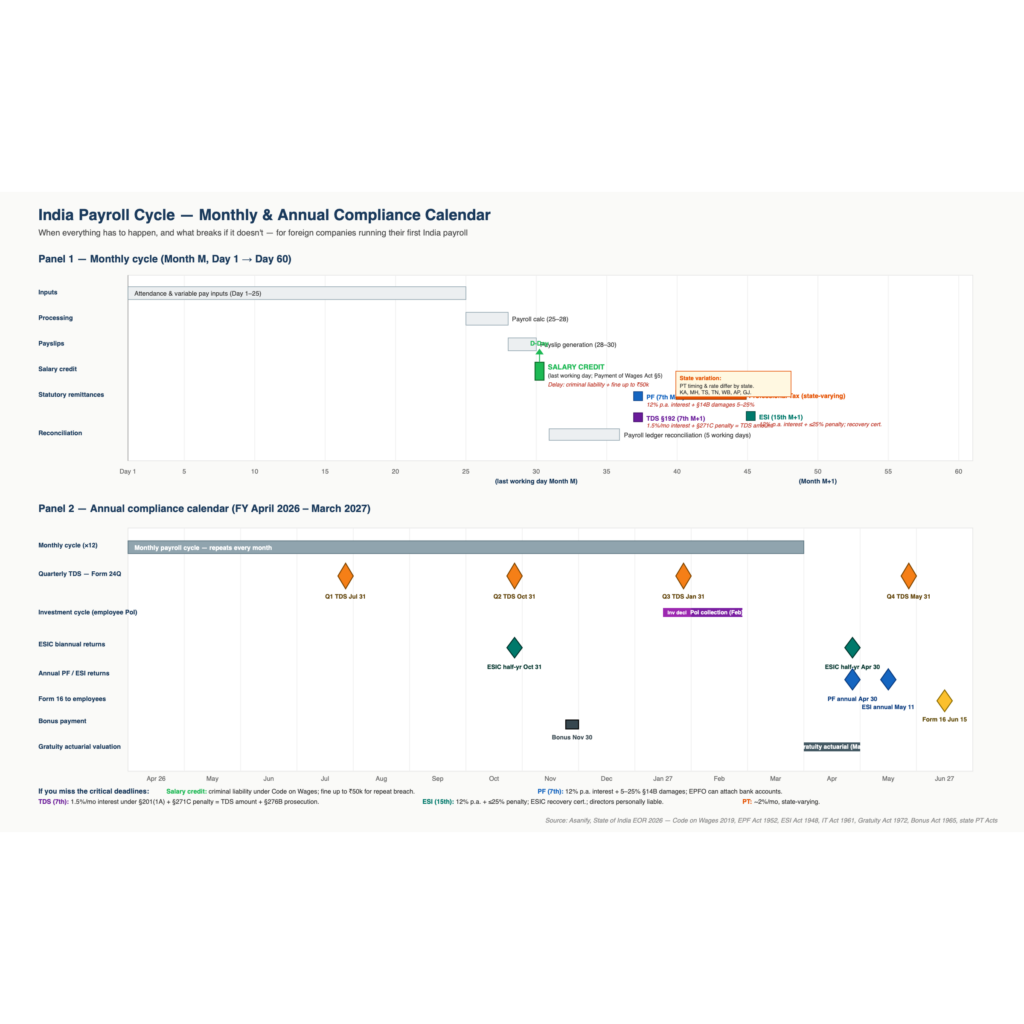

For a Series B–D US company that hired its first three “Indian contractors” in 2023 on an Upwork-style consulting agreement, the amnesty is the last cheap exit. Once it closes, the statutory baseline reasserts itself: Section 7Q of the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952 imposes simple interest at 12% per annum on any overdue contribution from the date it became due until the date of actual payment (Section 7Q, EPF & MP Act 1952 via Indian Kanoon). Section 14B of the same Act empowers EPFO to levy damages; following EPFO’s June 14, 2024 amendment, damages run at 1% per month — capped at 100% of arrears — replacing the older graded 5%-to-25%-per-annum schedule (AscentHR alert on the EPFO June 2024 damages amendment). Prosecution risk under Section 14 of the EPF Act runs alongside the recovery proceedings.

This section maps the doctrinal tests Indian courts apply, the new statutory category that the Labor Code consolidation has added, the enforcement infrastructure visible in the public record, and the specific double exposure — misclassification plus permanent establishment — that catches foreign companies hiring Indian “consultants.”

The tests an Indian court might apply

There is no statutory definition of “employee versus independent contractor” in Indian law. The question is litigated case-by-case under a body of Supreme Court precedent that has been remarkably consistent for two decades.

The controlling authority is Sushilaben Indravadan Gandhi v. New India Assurance Co. Ltd., AIR 2020 SC 1977, decided 15 April 2020 by R.F. Nariman and S. Ravindra Bhat, JJ. (Indian Kanoon doc/127871825). The case involved a surgeon engaged as an “Honorary Ophthalmic Surgeon” under a contract titled “Contract for Services.” When he died in a road accident in the institute’s minibus, the insurer denied liability under an employee-exclusion clause. The Court held he was an independent professional — but more importantly, it laid down the test that now governs every misclassification dispute in India.

The Court’s holding was that “no single test determines employment status. Instead, courts must apply a conglomerate of all applicable tests” considering control (whether the principal directs not just what work is performed but how), integration (whether the work forms an integral part of the business or remains merely accessory), remuneration (wages by time versus payment by results), tools and assets (who owns the equipment and bears financial risk), economic reality (whether the worker operates as an independent businessperson or depends on the principal for subsistence), and mutuality of obligation (fixed hours, mandatory attendance, termination mechanisms). The Court summarised this as the “economic reality test” and explicitly said “the level of control required is fact-specific and cannot be determined by a rigid formula.”

Sushilaben builds on Workmen of Nilgiri Coop. Mkt. Society Ltd. v. State of Tamil Nadu, AIR 2004 SC 1639, (2004) 3 SCC 514, decided 5 February 2004 (Indian Kanoon doc/1506370). Nilgiri stated the prior version of the same multi-factor framework: “No single test — control, organisation, or other — is determinative. Courts must examine: (a) appointing authority; (b) paymaster; (c) dismissal power; (d) service duration; (e) control extent; (f) job nature; (g) establishment type; (h) rejection rights.” Nilgiri found in favour of the principal — the 407 graders and porters were not employees — which is the right reminder that the test cuts both ways. A well-structured contractor relationship survives.

The practical effect of Sushilaben is that the label on the agreement does not control. A contract titled “Independent Consulting Agreement” gets pierced when the underlying relationship has enough indicia of employment — full-time exclusive work, daily standups, company laptop, fixed monthly payment, integrated reporting line. The Indian court will look through the form to the substance, and the burden of proof rests on the party claiming employer-employee status (Nilgiri).

The new third category: gig and platform workers

The Code on Social Security 2020, in force from 21 November 2025, introduces statutory definitions for “gig worker” and “platform worker” that did not exist in earlier Indian labour law (see Chapter I definitions). PRS Legislative Research summarises the definitions verbatim: a gig worker is “a person who performs work or participates in a work arrangement and earns from such activities outside of traditional employer-employee relationships,” and platform work is “a work arrangement outside of a traditional employer-employee relationship in which organisations or individuals use an online platform to access other organisations or individuals to solve specific problems or to provide specific services, or any such other activities which may be notified by the Central Government, in exchange for payment” (PRS Legislative Research, Code on Social Security 2020; cross-verified Mondaq, Khaitan & Co commentary). The Code’s Schedule 7 lists nine categories of “aggregator,” including ride-sharing, food and grocery delivery, content and media services, and e-marketplaces. The notification number for the 21 November 2025 in-force date is tracked at MoLE’s implementation page and the EY tax alert on the four-codes commencement.

The funding architecture is what should concern foreign payers: schemes are funded through contributions from the central government, state governments, and aggregators, at 1-2% of annual turnover, capped at 5% of amounts paid to gig/platform workers (PRS Bill summary). Neither PRS nor the Khaitan/Mondaq commentary cites the specific section number, and indiacode.nic.in returned 403 across re-fetch attempts; the language above is consistent across both secondary sources.

For a foreign company routing India hires through a “freelance” contract paid via Wise, Payoneer, or a vendor’s contractor-pay product, the practical question in 2026 is no longer the binary “employee or contractor” — it is whether the work fits the gig-worker / platform-work definition, which carries its own contribution obligation that does not depend on the Sushilaben employee test. The Code creates a third bucket that the old contract-of-service / contract-for-service framework was not designed to anticipate.

EPFO and ESI back-claims: the recovery mechanics

Once the amnesty closes, EPF recovery on a misclassified contractor runs on the statutory baseline above — 12% simple interest under Section 7Q plus damages under Section 14B at the post-June-2024 rate of 1% per month capped at 100% of arrears. ESI runs an analogous mechanism under the ESI Act 1948. Where the principal employer relationship is established under the Contract Labour (Regulation and Abolition) Act, 1970, the principal can be held liable for PF on the contractor’s workers — the Bombay High Court reinforced this on February 27, 2024 in Matheran Municipal Council v. Assistant Provident Fund Commissioner, holding that the principal employer carries the obligation to maintain records and pay statutory dues for contract workers where the contractor defaults (Legitquest case page). Beyond PF/ESI, misclassification rulings carry collateral exposure on TDS (Section 192 if employee versus Section 194J if professional — wrong withholding plus interest), gratuity once five years of “continuous service” is established, and bonus under the Payment of Bonus Act.

The wider wage definition imported by the four codes notified on 21 November 2025 — where HRA, conveyance and other excluded heads above 50% of gross now count as wages for PF — pulls more India hires into PF coverage at a higher contribution base. A contractor who could plausibly have been argued out of PF under the old wage definition has a thinner defence under the new one.

State and tribunal enforcement: what’s on the public record

Specific notice-quantum statistics for state labour-commissioner action are not in the public record at the granularity reported in U.S. wage-and-hour enforcement . What is visible is the doctrinal direction. The Bombay High Court’s Matheran ruling above is the recent named authority on principal-employer PF liability for contractor workers. Karnataka has published the Karnataka Platform Based Gig Workers (Social Security and Welfare) Draft Bill, 2024 (PDF item 37, dated 29 June 2024) — a state-level statute that would impose a welfare-fee levy on aggregators operating in Karnataka, on top of the central Code on Social Security. Maharashtra and Telangana have followed similar drafting tracks per Dentons Link Legal’s May 2025 Labour and Employment Newsletter. The contract-labour registration threshold in Karnataka is 20 or more workers — below the threshold, the principal-employer obligations under the Contract Labour Act do not engage, but the Sushilaben employee test does. The threshold is jurisdictional, not substantive.

The consultant trap (cross-reference to B1)

The most common contractor-trap pattern foreign companies fall into in India: a “consultant” in Bengaluru on a $4,000/month invoice, working full-time exclusively for the US parent, on a US-issued laptop, attending the US engineering standup at 9pm IST. Under Sushilaben, this is an employee on the economic-reality and integration prongs. Under the Code on Social Security, the platform-work category does not save them — there is no online platform mediating the engagement; the US company is the direct principal. The contractual label “Independent Contractor” loses.

The compounding exposure is to permanent establishment (covered separately in this report at B1). The same facts that make the consultant a misclassified employee under labour law — fixed remuneration, exclusive service, integration into the parent’s organisation, principal direction — are the facts an ITAT bench reads as constituting a fixed place of business or dependent agent under Article 5 of the India-US DTAA. A single mischaracterisation triggers both income-tax PE exposure on the parent’s India-source profits and EPF/ESI back-claims on the worker. The cost is asymmetric: the EPF back-claim is a multi-lakh-per-consultant-year exposure; the PE finding can run an order of magnitude larger once the attribution exercise is complete.

🛠️ Run the check on your India contractor. Asanify’s free 4-minute Misclassification Risk Quiz scores your engagement against the EPF Act §2(f), Code on Social Security 2020, and the Sushilaben/Hussainbhai line of cases — and outputs a tier-based risk rating with an EPF back-claim exposure estimator. Start the misclassification check →

Contractor conversion. Asanify converts contractor engagements to compliant Indian employment under a contract of service. The conversion addresses the Section 17(c) IP vesting question covered in Section B3 and removes the worker from the contractor-versus-employee economic-reality test for the forward engagement. Foreign principals planning a conversion of an existing contractor can request a pre-conversion engagement review (working hours, exclusivity, tools, reporting line, tenure) against the Sushilaben factors, with any pre-conversion EPF, ESI, or gratuity exposure flagged for the foreign principal’s own tax counsel to size. The review is operational triage to support the foreign principal’s own analysis, not a tax or legal opinion. Pre-conversion exposure is a function of the historical engagement pattern and is not eliminated by the forward conversion.

Clause patterns Indian tribunals treat as evidence of employment

Tribunals applying the Sushilaben and Nilgiri factors have repeatedly read the following clause patterns as indicia of an employment-like relationship rather than a true contract for services:

- Fixed monthly fee paid on the same date each month, regardless of deliverables or invoices submitted — characterised in the Sushilaben factor list as a “salary by another name” indicator on the remuneration prong.

- Exclusivity clauses preventing the contractor from working for other clients — mutuality-of-obligation factor in Sushilaben; Nilgiri test (f) “nature of work”.

- Defined working hours (“9am to 6pm IST” or “minimum 40 hours per week”) rather than deliverable-based engagement — Nilgiri test (e) “control extent”.

- Principal supplies all equipment — laptop, software licences, VPN credentials — the Sushilaben “tools and assets” prong.

- Notice-period termination rather than completion-of-deliverable termination — the longer the notice period, the more it resembles an employment contract.

- Confidentiality and IP-assignment clauses drafted as if for an employee — these are typically enforceable against contractors. Post-termination non-compete clauses, by contrast, face Section 27 of the Indian Contract Act 1872 (Indian Kanoon doc/1431516): Indian courts routinely void post-termination restraints regardless of whether the counter-party is an employee or a contractor.

- Reporting line into an internal manager with appraisal cycles, OKRs or performance reviews — direct evidence of integration under Sushilaben.

- Company-issued email address in the principal’s domain (

@parent.com) — tribunals have flagged this as one indicium of integration in the multi-factor analysis.

No single clause is individually fatal. The Sushilaben Court was explicit that the analysis is multifactorial. Two or three of these in a contract that runs for more than 12 months and pays a fixed monthly fee is the configuration tribunals find against the principal on.

Three questions to align with your EOR provider on contractor conversion

-

Engagement-pattern review. Will the EOR walk through your existing contractor’s working arrangement (working hours, exclusivity, tools, reporting line, tenure) against the Sushilaben economic-reality factors before formal conversion, and provide a written summary of what surfaces?

-

Pre-conversion exposure sizing. The Sushilaben test is fact-specific and the EPF, ESI, and gratuity back-claim quantum depends on wage history and tenure. How does the EOR work with your tax counsel to size pre-conversion exposure, and what data inputs does it expect from your side?

-

Forward-period statutory contributions. After conversion, when do statutory contributions begin? Confirm in writing that PF, ESI (where applicable), gratuity provisioning, and professional tax start from day one of compliant employment, not from the formal first payroll cycle.

B5. ESOPs and Equity for Indian Employees of Foreign Companies

TL;DR — B5: If you grant stock options to India EOR employees, they pay Indian income tax on the gain at exercise — in cash, before selling any shares. For a mid-senior engineer with significant options, this can be a six-figure rupee bill. India’s startup tax deferral mechanism is inaccessible to foreign-parented companies. Cash-settled stock appreciation rights (SARs) avoid the FEMA compliance layer entirely and may be the cleaner structure for EOR-hired employees.

A US-parented Series C company hires its first ten engineers in Bengaluru through an EOR. Three months later, the comp committee approves an option grant from the Delaware parent’s 2024 Stock Plan. The grant letter is identical to the one a New York hire would receive. At that moment the employer has just stitched together four regulatory regimes — three Indian, one global — and the EOR, who is the legal employer of record in India, is not a counterparty to any of the underlying grants and has no contractual relationship to the foreign parent’s equity plan. Whether it inherits withholding or reporting duties by default is the operative question.

This is the section the global EOR brochures do not write. The arbitrage-evaporation mechanism here is not in the salary line; it is in the cap table.

The four regimes a foreign-parent ESOP must navigate

Indian employees receiving stock from a foreign parent sit at the intersection of four bodies of law, each owned by a different regulator:

- FEM (Overseas Investment) Rules, 2022 — Ministry of Finance + RBI, notified August 22, 2022. Governs whether an Indian-resident individual may acquire foreign equity.

- RBI’s Liberalised Remittance Scheme (LRS) — caps how much foreign exchange the same individual may remit outward in a financial year.

- Section 17(2)(vi), Income Tax Act 1961 — taxes the exercise as a salary perquisite in the hands of the employee.

- Section 156(2) read with Section 192(1C), Income Tax Act 1961 (both inserted by Finance Act 2020) — narrow deferral mechanic for DPIIT-recognised, IMB-certified startups. Structurally inaccessible to foreign-parent grants.

Each regime has a different reporting form, a different filing entity, and a different consequence for non-compliance. None of them are designed around the EOR fact pattern.

FEMA OI Rules 2022 — the foreign-equity-acquisition gate

The 2022 OI Rules created an express ESOP carve-out for resident-employee acquisition of foreign-parent shares. The operative rule reads:

“A resident individual, who is an employee or a director of an office in India or branch of an overseas entity or a subsidiary in India of an overseas entity or of an Indian entity in which the overseas entity has direct or indirect equity holding, may acquire, without limit, shares or interest under Employee Stock Ownership Plan or Employee Benefits Scheme or sweat equity shares offered by such overseas entity, provided that the issue of Employee Stock Ownership Plan or Employee Benefits Scheme are offered by the issuing overseas entity globally on a uniform basis.”

The two operative phrases are without limit and globally on a uniform basis. The first removes the standard LRS cap for ESOP acquisitions. The second is what practitioners have read as the trap door: if the foreign parent grants on bespoke terms to its India hires that do not mirror the global plan, the carve-out fails. The acquisition then has to fit inside the ordinary OI Rules classification — ODI (Overseas Direct Investment) if 10% or more of paid-up capital with control, OPI (Overseas Portfolio Investment) otherwise — with corresponding Form FC and Form A-2 filings through an authorised dealer bank. Reporting for OPI falls on the Indian subsidiary or related entity on a half-yearly basis (September 30 and March 31 cut-offs).

For EOR-hired employees the related-entity reporting prong is precisely the friction point: there is no Indian subsidiary. The EOR is the legal employer; the foreign parent is the issuer; the OPI reporting hook has no obvious home. This is one of the few sub-topics where tier-1 Indian counsel advice has been to either (a) restructure the equity as a Stock Appreciation Right or phantom plan (cash-settled, no FEMA acquisition at all), or (b) have the foreign parent treat the EOR-hire grants as a residuary case requiring direct advisory engagement with the authorised dealer bank.

RBI LRS — what the carve-out actually does to the ceiling

Where the OI Rules ESOP carve-out applies, the LRS ceiling is functionally inoperative for ESOP acquisitions — that is the point of the “without limit” language. Where the carve-out does not apply (bespoke India-only terms, non-uniform vesting, materially different exercise mechanics from the global plan), the USD 250,000 per-financial-year LRS cap reverts to being the binding constraint. The Liberalised Remittance Scheme permits resident individuals to remit “up to USD 2,50,000 per financial year (April – March)” for permissible capital and current account transactions (RBI LRS FAQs, Id=1834;). The carve-out matters most for senior India hires whose option exercise costs run into hundreds of thousands of dollars — without it, a single exercise blows through the cap.

As a parenthetical: Budget 2025 raised the TCS threshold on outward remittances from ₹7 lakh to ₹10 lakh per FY, which softens the cash-flow hit but does not change the underlying ceiling. Cashless / sell-to-cover schemes are the cleanest path operationally because they minimise actual cash crossing the border in either direction; the employee never has to send dollars out, and the proceeds come back as portfolio income.

Section 17(2)(vi) — the cash-flow trap at exercise

The hard part of foreign-parent equity for Indian employees is not the foreign-exchange piece. It is the tax timing.

Under Section 17(2)(vi) of the Income Tax Act 1961:

“Taxable perquisite = Fair Market Value (FMV) of shares on exercise date − exercise price paid by employee” (Corporate Professionals analysis of Section 17(2)(vi);)

That spread is taxed as salary income in the year of exercise — subject to TDS under Section 192, payable in cash before selling any shares.

Illustrative impact — engineer exercises options at a $40 spread on 5,000 shares: – Perquisite: ~₹1.8 crore (~$2 million at ₹90/$) – Effective tax rate: ~39% (30% slab + 25% surcharge above ₹2 crore + 4% cess) – Tax bill: ~₹70 lakh (~$780,000) — due in the exercise year, before any share sale

FMV rules: – Listed parent: average of opening and closing price on the exercise date – Unlisted parent: merchant banker valuation within 180 days of exercise

The withholding hook falls on “the employer.” For a foreign-parent grant to an Indian employee who is on an EOR’s books, no party fits cleanly: the EOR did not issue the security, the foreign parent has no Indian payroll, the Indian subsidiary (if one exists) was not the grantor. In practice the EOR’s Indian payroll often becomes the withholding agent — running the perquisite through its India payroll on instruction from the foreign parent, with reimbursement flowing back through the service fee. The legal basis is unsettled: the EOR is not the grantor and Section 192 contemplates an employer-grantor relationship. The mechanic is workable when coordinated in advance among the foreign parent, the foreign parent’s equity plan administrator, the EOR’s India payroll, and the worker’s tax adviser. The modal failure pattern is treating ESOP coordination as a question to resolve at first exercise rather than at grant approval.

Section 156(2) read with Section 192(1C) — the founder-friendly deferral that almost no one qualifies for

Finance Act 2020 inserted Section 192(1C) (TDS deferral) and Section 156(2) (deferral of the demand-notice timing) to give DPIIT-recognised, IMB-certified startups a 48-month perquisite-tax deferral. The Section 156(2) text reads that the tax “shall be payable by the assessee within fourteen days” of the earliest of:

“(i) after the expiry of forty-eight months from the end of the relevant assessment year; or (ii) from the date of the sale of such specified security or sweat equity share by the assessee; or (iii) from the date of the assessee ceasing to be the employee of the employer.”

Section 192(1C) imposes a parallel 14-day window on the employer’s TDS obligation, triggered by the same three earliest events (taxguru.in analysis of Sections 156(2) and 192(1C), Income Tax Act, as inserted by Finance Act 2020;). Note the sub-parts are numbered (i)/(ii)/(iii), not lettered — earlier drafts of this section cited “Section 156(7)(c),” which does not exist in this context; the correct subsection is 156(2).

The funnel is brutally narrow. Per the Startup India portal, eligibility requires both DPIIT recognition AND IMB certification under Section 80-IAC (Startup India portal;). Public official reporting showed more than 3,700 startups approved under the §80-IAC (IMB) regime as of May 2025 (per official Government reporting on the 79th and 80th IMB meeting approvals ), against more than 2.23 lakh DPIIT-recognised startups as of 31 March 2026 (DPIIT ) — implying fewer than 2% of recognised startups qualify for ESOP tax deferral under this route.