The short version: Hiring in India through an Employer of Record does not automatically create a permanent establishment (PE), and it does not automatically shield you from one. PE risk turns on conduct, mainly whether someone in India habitually concludes contracts on your behalf. Six 2025–26 Indian rulings tightened the test. keep contract authority with your home entity and the risk stays low.

If your company has engineers, sales staff, or operations people working in India, through an Employer of Record (EOR), contractors, or a small local team, one tax question decides whether India can tax a slice of your global profits: have you created a permanent establishment in India? The stakes are real. In February 2026 an Indian tribunal set aside a ₹3,960 crore (about US$475 million) tax demand against Booking.com that turned entirely on whether it had a PE in India. The line moved six times in eighteen months. Here is where it sits now, and what foreign companies hiring in India through an EOR should actually do about it.

What “permanent establishment risk” means

Permanent establishment is the trigger, under every double-tax treaty India has signed, that lets India tax a foreign company’s business profits. No PE, and India generally cannot tax your profits. A PE, and a portion of your global income becomes taxable in India, often with penalties and interest on top. “Permanent establishment risk” is the exposure that an arrangement you think is safe, a few remote hires, a local agent, an EOR-employed team, is later recharacterised as a taxable presence.

Three forms of PE matter most when hiring in India:

- Fixed-place PE — a fixed location (an office, or even continuous use of someone else’s premises) through which your business is carried on.

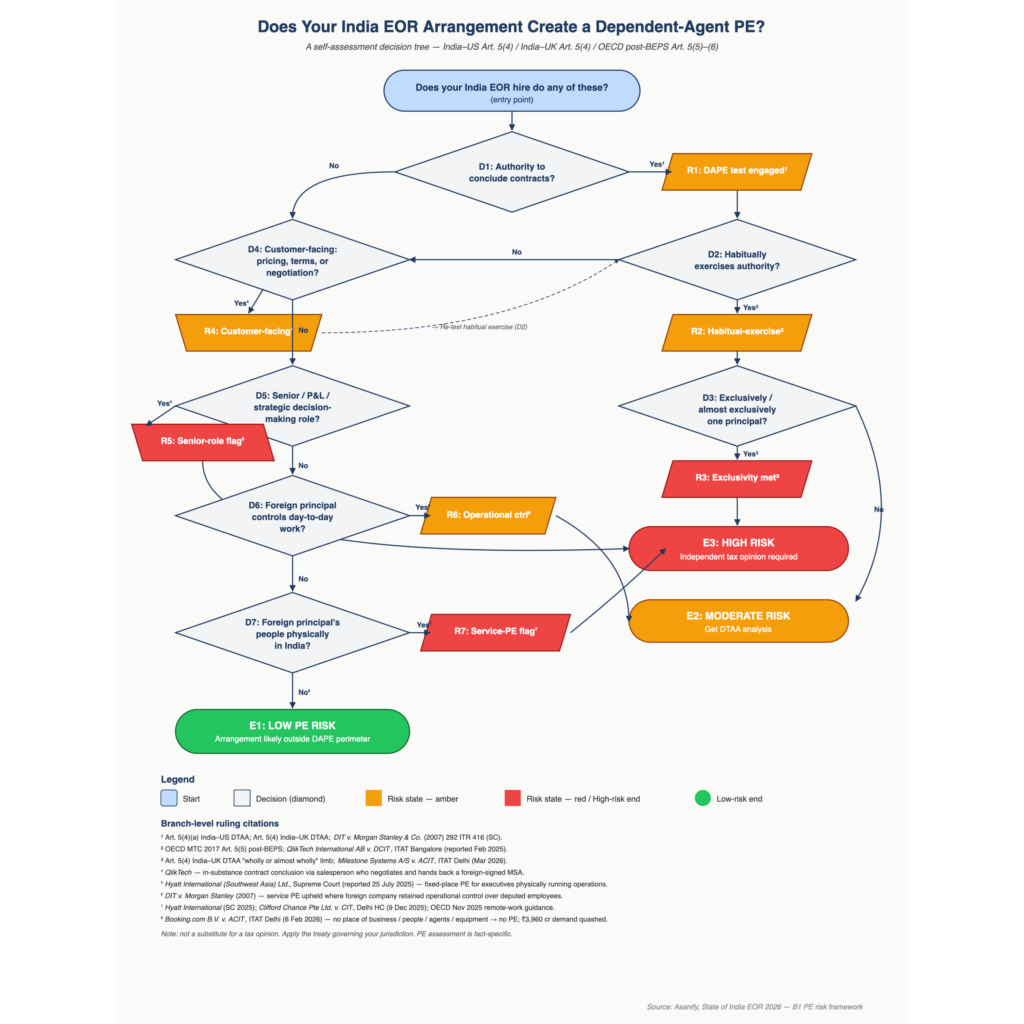

- Dependent-agent PE (DAPE) — a person in India who habitually exercises authority to conclude contracts on your behalf. This is the one EOR and remote-hiring setups most often trip.

- Service PE — services furnished in India through personnel beyond a treaty threshold of days.

Does an Employer of Record create, or shield you from, permanent establishment?

Indian EOR providers have marketed a clean promise for years: “use an EOR and you are protected from permanent establishment.” That answer is too clean. Whether you have a dependent-agent PE depends on what the person in India does, not simply whose payroll they sit on.

An EOR does help. It is the legal employer, so the individual is not your employee, and a well-drafted EOR engagement keeps contract-concluding authority out of India. But if your India-based person habitually negotiates and concludes contracts that bind your company, the dependent-agent PE test can still be met. The Supreme Court framed it in DIT v. Morgan Stanley (2007): a PE arises where a person “other than an agent of an independent status habitually exercises an authority to conclude contracts on behalf of the assessee.” An EOR changes the employment relationship. it does not, by itself, change who concludes your contracts.

The practical test: an EOR reduces fixed-place and employment-law exposure, but PE risk is mostly about authority and conduct in India. Keep contract-signing, pricing, and deal-closing authority with your home entity and the dependent-agent PE risk drops sharply.

The 2025–26 rulings that moved the line

Between July 2025 and March 2026, six Indian tribunal and Supreme Court decisions redrew the boundary between a safe arrangement and a taxable PE:

| Ruling | Court & date | What it established |

|---|---|---|

| Hyatt International | Supreme Court, Jul 2025 | Continuous, systematic use of another entity’s premises can create a fixed-place PE, even without a lease or owned office. |

| Booking.com B.V. | ITAT Delhi, Feb 2026 | A ₹3,960 crore demand set aside. genuine third-party Indian arrangements need not be a PE. |

| QlikTech / Milestone Systems | ITAT Bangalore Feb 2025 / Delhi Mar 2026 | Dependent-agent PE turns on whether the Indian entity acts as an independent principal or a dependent agent. |

| CIT v. Clifford Chance | Delhi HC, Dec 2025 | Service-PE exposure can arise once personnel cross the treaty physical-presence threshold. |

| RGA International | ITAT Mumbai, Jul 2025 | Anti-fragmentation: you cannot split activities across entities to stay under the PE threshold. |

Taken together, the rulings reward substance and clean structure and punish arrangements that look like a disguised Indian presence. For the full six-ruling analysis, the four-test framework, and the treaty texts behind them, with every case linked to its primary source, see the deep dive in our research report.

Read the full PE analysis in State of India EOR 2026 →

How to reduce permanent establishment risk when hiring in India

- Keep authority to negotiate and conclude contracts with your home entity, not your India staff.

- Hire through a structured Employer of Record in India so the individual is the EOR’s employee and the engagement is documented.

- Avoid giving India-based staff a fixed office or premises that function as your place of business.

- Document roles so India activities are support, research, or back-office, not the core revenue-concluding function.

- Check the specific treaty for your home country. the dependent-agent and service-PE language differs by treaty.

Not sure where your India setup sits?Run the free 60-second check, no email required, or talk it through with a specialist.

Take the PE Risk Quiz →Consult an India EOR expert →

Frequently asked questions

Not by itself. An EOR makes the worker the EOR’s legal employee, which removes much of the fixed-place and employment exposure. Permanent establishment risk mainly turns on whether someone in India habitually concludes contracts on your behalf, keep that authority at home and the dependent-agent PE risk is low.

A dependent-agent PE arises when a person in India who is not an independent agent habitually exercises authority to conclude contracts for a foreign enterprise (the test from DIT v. Morgan Stanley). It is the most common PE trigger for remote and EOR-based India teams.

It can, if their activities amount to carrying on your business in India, especially concluding contracts or providing services beyond treaty thresholds. Support, engineering, and back-office roles carry lower risk than revenue-closing roles.

Six tribunal and Supreme Court decisions tightened the analysis. The Hyatt ruling expanded fixed-place PE to continuous use of premises, while Booking.com confirmed that genuine third-party arrangements need not be a PE. Substance and clean structure matter more than ever.

Not to be considered as tax, legal, financial or HR advice. Regulations change over time so please consult a lawyer, accountant or Labour Law expert for specific guidance.