As an employee, you must submit an investment declaration proofs before the end of the year (or by January latest). Now, what is an investment declaration? It is a document in which you provide your investment proposition and then will provide proofs for at year end. In this blog, I will be talking about all you need to know about investment declaration and how the taxes will be calculated and deducted in your payroll.

- What does investment declaration consist of?

- What is Form 12BB for investment declaration?

- Why is investment declaration important?

- How can employers verify supporting documents?

- What is the mode and time of submission for investment declaration?

- How to Empower and enhance employee’s experience through payroll?

- What is Investment Proof for investment declaration?

- Important Tax Saving Investment/Expenditure Proofs.

- Why You Should Never Forget to Submit Your Investment Declaration Form?

- Which are the Common Mistakes While Submitting Investment declaration?

- What happens at the end of the tax year?

- What is the Investment Declaration Procedure Under the New Tax Regime?

- Is Form 12BB Applicable to the New Tax Regime?

- FAQ

What does investment declaration consist of?

1. House Rent Allowance (HRA)

In the first part of Form 12BB, you can fill the details required to claim tax deduction on HRA.

To claim HRA, you need to provide details such as:

- Name and address of landlord and actual rent paid.

- If the rent paid during the year exceeds Rs. 1 lakh, you also need to provide a PAN of the landlord.

- Rent receipts. (In case, if you are paying the rent by cash, you have to affix a revenue stamp on the receipts).

2. Leave Travel Concessions or Allowance (LTC/LTA)

- Leave travel concession or leave travel allowance is paid to a salaried employee as per salary package and is applicable for domestic travel only.

- Salaried employees also need to submit travel related expenditure proofs to their employers if they want to claim tax deduction on LTA/LTC.

- The total expenditure being claimed as well the number of documents being submitted should be mentioned in Form 12BB.

3. Interest on Home Loan

To claim tax deduction on interest paid for home loan, you also need to provide details like interest paid /payable, lender’s name, lender’s PAN in Form 12BB.

Stamp duty, registration fees and brokerage expenses paid towards transfer of the property can be claimed as deduction.

4. Deductions under Section 80C, 80CCC, 80CCD and 80D

Here is a quick list of deductions available under Section 80 that you can declare in Form 12BB.

- 80C: Premium to be paid for life insurance and/or investments to be made in ELSS funds, PPF, NPS and/or school tuition fees for children, etc.

- 80CCC: Premium to be paid for annuity plan.

- 80CCD: Additional contributions made to NPS.

- 80D: Premium to be paid for medical insurance.

- 80DD: Expenses incurred for the treatment of dependents who are physically challenged

- 80E: Interest to be paid on education loan.

- 80EE: Deduction can be claimed against a housing loan (applicable if you are owning a home for the first time)

- 80G: Donations to be made to specified organizations.

- 80GG: Rent charges to be paid for accommodation if HRA is not being received from employer

- 80GGA: Donations made to any organization engaged in scientific research and development of rural areas

- 80GGC: Any kind of non-cash donations made to political parties

- 80TTA: Deduction up to Rs 10000 for interest income earned from savings bank account. However, the same is not applicable to term deposits interest

- 80U: Maximum rebate of Rs 1.25 lakhs is available if a physically challenged employee claims for it (depending on their disability)

Also Read: 10 Tax saving tips you can benefit from today!

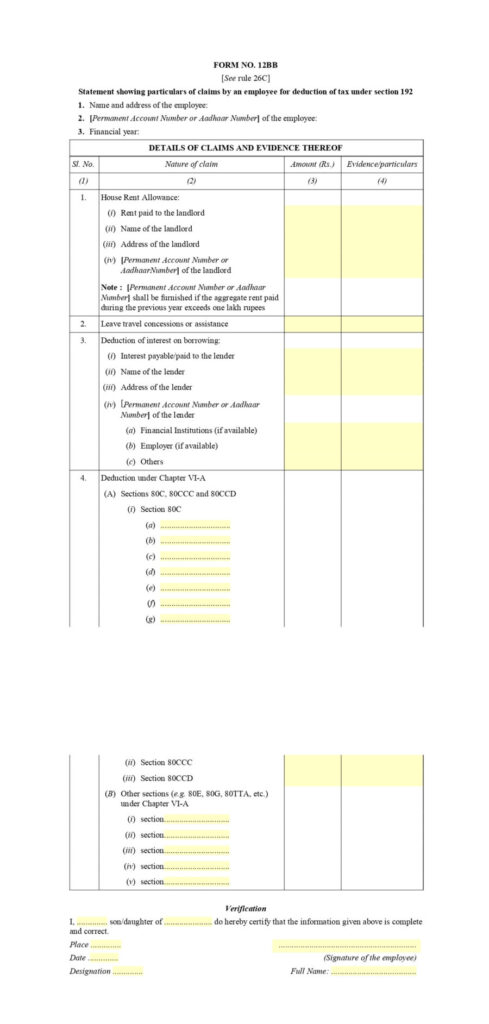

What is Form 12BB for investment declaration?

The Form 12BB is also an assertion of cases by a representative for allowance. With impact also from first June 2016, a salaried employee is needed to present the Form 12BB to their employer to guarantee tax reductions or refund on ventures and costs. Form 12BB must also be submitted toward the end of the financial year.

Form 12BB applies to all salaried citizens. Using Form 12BB, an employee needs to announce the ventures that they have made during the year. Narrative proof of these speculations and costs must also be given toward the end of the financial year.

Suggested Read: Types of Employment Contracts

Sample of Form 12BB for investment declaration

Why is investment declaration important?

- As per the law, a business needs to deduct charge at source on the assessed pay of the worker consistently.

- Before Union Budget 2020, the Income Tax Act permitted workers to guarantee certain costs and ventures and diminish their taxation rate.

- In Union Budget 2020, the public authority presented another assessment system with lower charge pieces, yet with less exclusions and allowances. Nonetheless, workers are allowed to think about and choose the good system dependent on their pay.

- To pick the most ideal choice, workers need to make charge affirmations and figure their expense liabilities.

- When the choice is made, managers can deduct annual expense from the employees’ salary.

How can employers verify supporting documents?

Employers provide a cut-off date for submission of investment or expense proof. Usually, this date lies in January or February, so that shortfall of taxes is recovered in the remaining months of the financial year.

Here’s the table for verification tips for employers for the most popular tax-saving investments:

Investments |

Description |

Documents to collect |

Important Points |

House Rent Allowance (HRA) |

For most employees, HRA is also a part of their salary structure and provides benefits for the rental expenses made during the year. The benefit amount available to employees is the least of the following:

|

Rent receipts |

The rent receipts can be monthly/ annually. If the rent paid is higher than Rs 1 lakh in a year, owner’s PAN is mandatory. |

Leave Travel Allowance (LTA) |

|

Tickets for domestic travel and also boarding pass in case of air journey. | Applicable to only domestic travel expenses. |

Housing Loans EMIs |

|

|

Declaration should also indicate borrowers and share of ownership. |

Life Insurance Premium |

LIC premium paid during the year can also be claimed as deduction under section 80C, up to a maximum of Rs. 1.5 lakh. | Receipts of premium paid. |

|

Public Provident Fund (PPF) |

Employees can also invest in a PPF account. Claim up to Rs 1.5 lakh in a year under section 80C. | PPF account statement or passbook. | Either statement or passbook should have the account details.

Also transfer record showing the amount along with the date of investment. |

Children Tuition Fees |

Any amount paid towards children’s education can also be claimed under section 80C, up to a maximum of Rs 1.5 lakh. | School fees receipts. |

|

Medical Insurance |

Medical insurance premium for self and family. | Receipts of premium paid. | Premium payment should be made by the employee only.

Any amount paid, other than also for preventive health check-up, should be in electronic form. Medical bills for senior citizen parents can be claimed if there is no active insurance plan for them. |

What is the mode and time of submission for investment declaration?

In most companies, the collection of investment proofs is a manual and menial process. In your company if you do this manually, you need to store the physical copies of the proofs across 100s of employees. Later if and when your auditor asks for a proof, you might need to retrieve these documents and provide the same. A good payroll software such as Asanify simplifies this whole process by empowering employees self-submit the proofs online. Additionally, there is a built in workflow approval engine that enables managers to approve or reject the proof values. Moreover, this is all in a beautiful easy to use and delightful interface.

How to empower and enhance employees’ experience through payroll?

Don’t you think that work needs to feel wonderful? If an employee has to spend hours submitting tax declarations, that’s valuable time wasted. Moreover, this time could have been used productively to build your business. A smart payroll software automates this whole process. Asanify even gamifies the experience for employees and lets them save taxes.

What is Investment Proof for investment declaration?

Investment proof is the actual proof employees must submit to claim income tax deductions. There fixed rules laid down by the Department of Income Tax, India. These rules define how much income tax deduction the employee can get.

All employers are needed to save this proof for the following 6 years. Storing these items manually or even digitally across emails or whatsapp may cause a lot of problem. As a small business leader, please consider keeping all such documents in a central location. Otherwise you may store all such information in a payroll software.

As a payroll admin, you need to deduct taxes from your employees’ payroll monthly. These taxes depend on the deductions as per employee declarations.

How Does the Investment Proof Verification System Work?

The Investment Proof Verification System operates as follows:

- Every employee receives an email about the submission of their proof of investment.

- A local payroll provider can then verify uploaded proofs online and accept or reject the submissions.

- Employers can export the information in MS Excel and the payroll provider imports it into the payroll system for further calculation of salaries.

- In a payroll software, all these can be done online.

Important Tax Saving Investment/Expenditure Proofs

- Investments – Under Section 80C

For investments such as:

- Equity Linked Savings Schemes (ELSS) of mutual funds (MFs)

- Life insurance

Submit the ELSS fund statement and premium paid receipts respectively.

- Public Provident Fund (PPF) when maintained with a bank or a post office, you must submit photocopies of the passbook showing all the transactions and the account details.

- If maintaining PPF online, you must take a printout of the e-receipt showing transactions and the account details.

-

Tuition fees

With tuition fees, you must submit photocopies of the school receipt with the schools’ seal and signature of the receiver.

-

First-time home buyers

For loans sanctioned between 01-Apr to 31-Mar, Section 80EE also allows tax benefits for first-time home buyers under which the benefit can be claimed on home loan interest. This deduction is also over and above the INR 2 lakh limit under Section 24 of the Income-tax Act. Hard copies of all the relevant documents must be submitted.

-

House Rent Allowance Exemption

For those who claim HRA relief, the Permanent Account Number (PAN) of the landlord is also mandatory. This condition is not applicable for those whose rent payment is less than or equal to INR 1 lakh per annum, i.e., INR 8,333 per month. A copy of the lease rent agreement or declaration by the landlord in a prescribed format is also to be submitted. Further, ownership proof of landlord of rented premises, which can be house tax receipt or the latest electricity bill or share certificate in case of co-operative society houses have to be submitted. The original rent receipts for the period April till date must be provided.

-

Housing loan repayment (principal) for investment declaration

The certificate from a financial institution specifying the principal paid during April to March needs to be submitted also. Ask the institution to mention the provisional amount for the last 2-3 months of the current financial year as equated monthly installments (EMIs) would still be pending.

-

Loss from housing property – interest on housing loan – self occupied

The interest certificate from the bank or financial institution, also specifying the break-up of interest and the principal amount. Possession/construction completion certificates are a must for availing the relief by some employers. Further, the date the loan was taken and the date of possession are mandatory to avail the benefit.

-

Loss from housing property – interest on housing loan – let out on rent

If the house for which loan has been availed is let out, the same should be submitted with a certificate from a financial institution specifying principal and interest paid during April to March

-

New Pension Scheme (NPS)

There is no need to submit proof of actual Investments in case the investments in NPS is through Corporate Model or Employee Model as the same are recovered and deposited by the company in your PRAN (Permanent Retirement Account Number) account. However, if you have opted for investment of INR 50,000 under NPS on your own, i.e., outside salary, then submission of copies of PRAN card, NPS Transaction Statement for Tier 1 Account is necessary.

-

Mediclaim premium for investment declaration

Call up the insurer and also ask him to send the statement for tax purpose under Section 80D. The premium should also not be paid by cash and should be paid by cheque or digital transfer from the bank account.

Why You Should Never Forget to Submit Your Investment Declaration Form?

As an employee you stand to lose a lot of taxes if the declarations are not given on time. Additionally many companies mandate a cut off time for actual proof submissions. Further, if the proofs do not tally then the entire deductions are ignored and employee bears a large amount of tax.

If you have not declared your investments before and your employer has deducted excess TDS, then you can claim refund of excess TDS deducted by filing your income tax return.

Which are the Common Mistakes While Submitting Investment declaration?

Investment proof submissions are time consuming and manual. To prevent prolonging the process, avoid the common mistakes listed below.

1. Financial Planning

As an employee, you need to plan the annual investments at the beginning of the year. You may consult your personal accountants for advice. Asanify payroll is unique in the sense that it provides a gamified interface to evaluate the exact tax saving possible under each tax head.

2. Photocopy of investment proof

The Employee must keep the copies of investment proof if they work in a manual payroll system. In case of audit from Income tax office – these will be required. Otherwise for automated payroll software, the proofs may be digitally stored.

3. Reimbursement bills or invoice

Employees must follow the organization rules to submit expense reimbursement requests. In the event that the employee neglects to do as such, at that point a similar compensation part will be taxable and the organization will tax it.

4. Future Investment

The last date of Income Tax Investment Proof accommodation with the employer is typically January 15. This is because the tax implication may be such that the Jan, Feb and March salaries may need to be sufficiently reduced. This happens when the employee cannot provide appropriate proofs of the investments. Thus the amount you previously deducted for tax – for April to December may now need to be clawed back across the 3 remaining months.

Additionally, there is a chance that the employee needs to make more investments at later date. As an admin, you should ideally create a clear communication so that employees can submit proofs well on time. For this situation, the employee also needs to inform the employer about all such future investments. In light of employee assertion, the employer considers them for tax allowance purposes. Hence, an employee ought to present a presentation so they can be considered by their employer. Otherwise, they will also miss the tax advantage.

5. Avoid last minute rush

A little error in the submission of Income Tax Proof may also cause significant delay. The employee should pay attention to this cycle. Typically small business admins take 30 days time to finish verification of all these proofs. In Asanify’s experience, up to 80% of employees submit proofs on the last day. It’s important that employees also give the finance group adequate chance to check proofs. On account of any mistakes, they will at that point have sufficient chance to caution the employee and redress it.

Additionally note that verifying all the investment proofs across 100s of employees is a time consuming process. A full service payroll provider such as Asanify does this automatically. This frees up your finance and leadership to grow your business instead of doing these manual work. Asanify uses a mixture of AI to automatically read expense images and manual checks to do this in a foolproof way.

What happens at the end of the financial year?

Toward the end of the tax year, employees will be given a Form 16. It is given to the employee in the period of May or June each year.

The employee can get all the Income details they received from their employer in the last financial year alongside TDS credited to their account throughout the year.

In the event that the employee had various employers in the financial year; the employee will get a different Form 16 from every employer for the period which they worked for every employer. Form 16s are key records for employees to document their yearly Income Tax documenting, which should be submitted before July 31st (typically) every year.

At the point when a Form 16 is being given, a ‘Digital Signature Certificate’ (DSC) of approved signatory for each Form 16 is also required. A Digital Signature Certificate is also a protected advanced key; that is given by the affirming specialists also to approve and checking. Digital Signatures also utilize the public key encryptions for added security

Investment declaration is a great way for employees to save significant taxes. Additionally, for startups and small businesses this may require a lot of supervision and additional effort. Using an automated payroll software can save 100s of hours of manual work.

What is the Investment Declaration Procedure Under the New Tax Regime?

To break things down, the new tax regime is just a more simplified version of the older one. The core fact is that it offers a lower tax rate while removing exemptions from the older scheme at the same time. All one needs to do is submit Form 12BB declarations to their employers. It is important to note that employees can claim rebates under Section 87A till Rs 25,000 and the standard deduction of Rs 50,000.

Is Form 12BB Applicable to the New Tax Regime?

As mentioned above, the new tax regime, introduced in 2020, is all about simplifying the older system. Employees opting for this new regime can’t claim exemptions in Form 12BB. However, it is important that they submit it. Apart from the deductions that can be claimed (as mentioned above), one of the core differences between the two regimes is this. Under the old regime, tax-free income stands at Rs 5.5 lakh. On the other hand, it is 7.5 lakh under the new tax regime. So yes, Form 12BB is very much crucial and submitting it is mandatory for employees.

FAQ

You can claim tax benefit on the interest paid on home loan and also on principal repaid.

To declare investment proof, submit a copy of your FD receipt or print out your FD receipt/statement from your bank website.

An investment declaration form is a provisional statement that has details about your proposed investments and expenses that are income-tax deductible.

At the end of the financial year, you need to provide supporting investment proofs for these investments that you have specified in the declaration form.

In order to get tax deduction, the investment proofs you require to submit include your document of :

1. Insurance premium.

2. Investments made in tax-saving mutual funds.

3. Health insurance premium receipt.

4. Receipt of donation.

Yes, you can claim income tax exemption on both house rent allowance (HRA) and repayment of home loan.

If you are living in a house on rent and servicing home loan on another property – even if both the properties are located in the same city – you can claim tax benefit for both.

Not to be considered as tax, legal, financial or HR advice. Regulations change over time so please consult a lawyer, accountant or Labour Law expert for specific guidance.